The Stablecoin Regulation Revolution: Senate’s “Genius Act” Reshapes Digital Finance

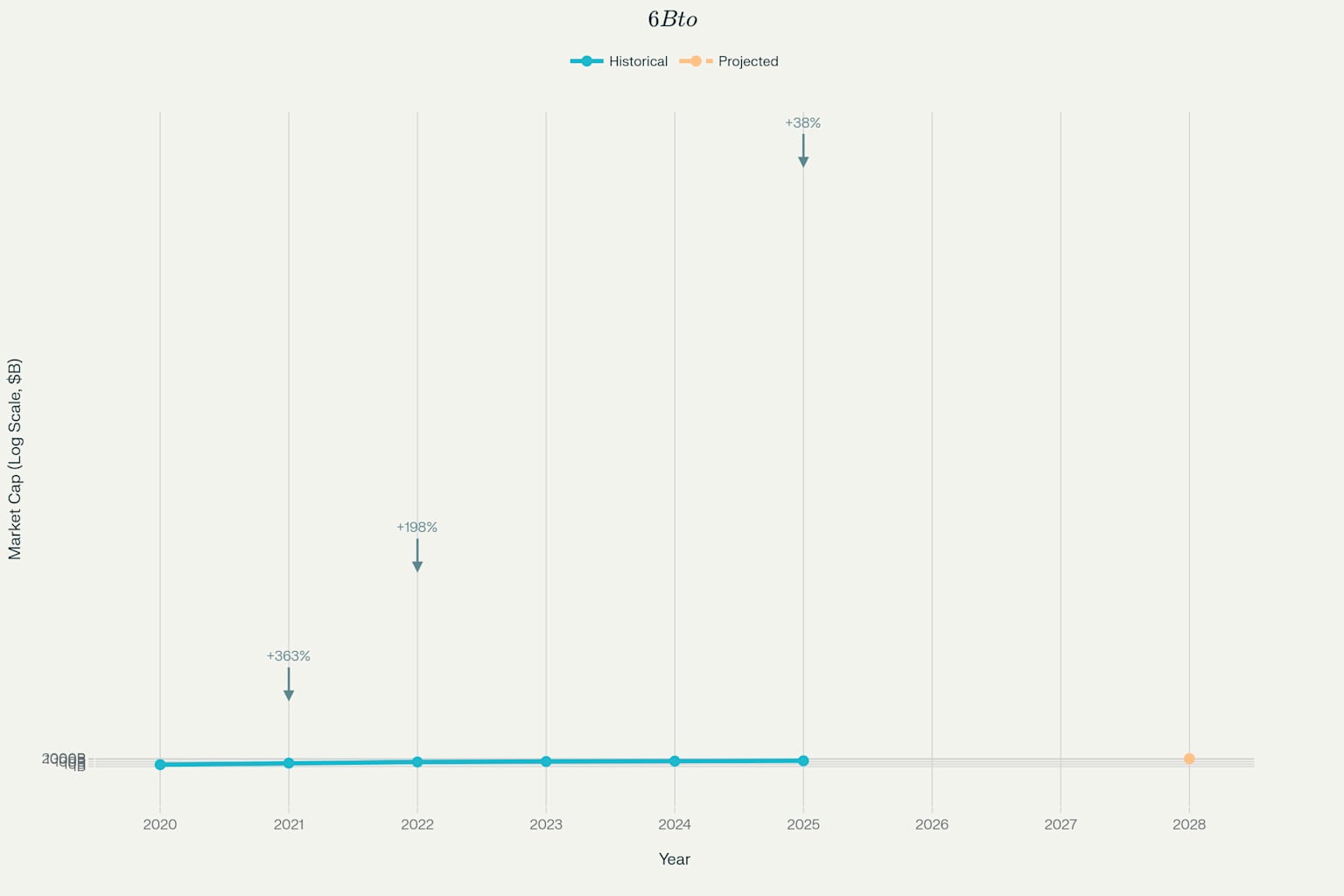

The United States Senate’s historic passage of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act on June 17, 2025, represents the most significant regulatory milestone in the cryptocurrency sector’s evolution, fundamentally reshaping the competitive landscape between digital assets and traditional banking systems. This landmark legislation establishes the first comprehensive federal framework for stablecoin regulation, addressing a $251.5 billion market that has surged from $5.9 billion in 2020 while processing $27.6 trillion in annual transaction volume that now exceeds the combined throughput of Visa and Mastercard.

The bipartisan 68-30 Senate vote signals a decisive shift from fragmented state-by-state oversight to coordinated federal regulation, creating new competitive dynamics that traditional banks and technology companies must navigate. Treasury projections indicate that the stablecoin market could reach $2 trillion by 2028, underscoring the economic significance of this regulatory transformation.

Market Dynamics and Current Landscape

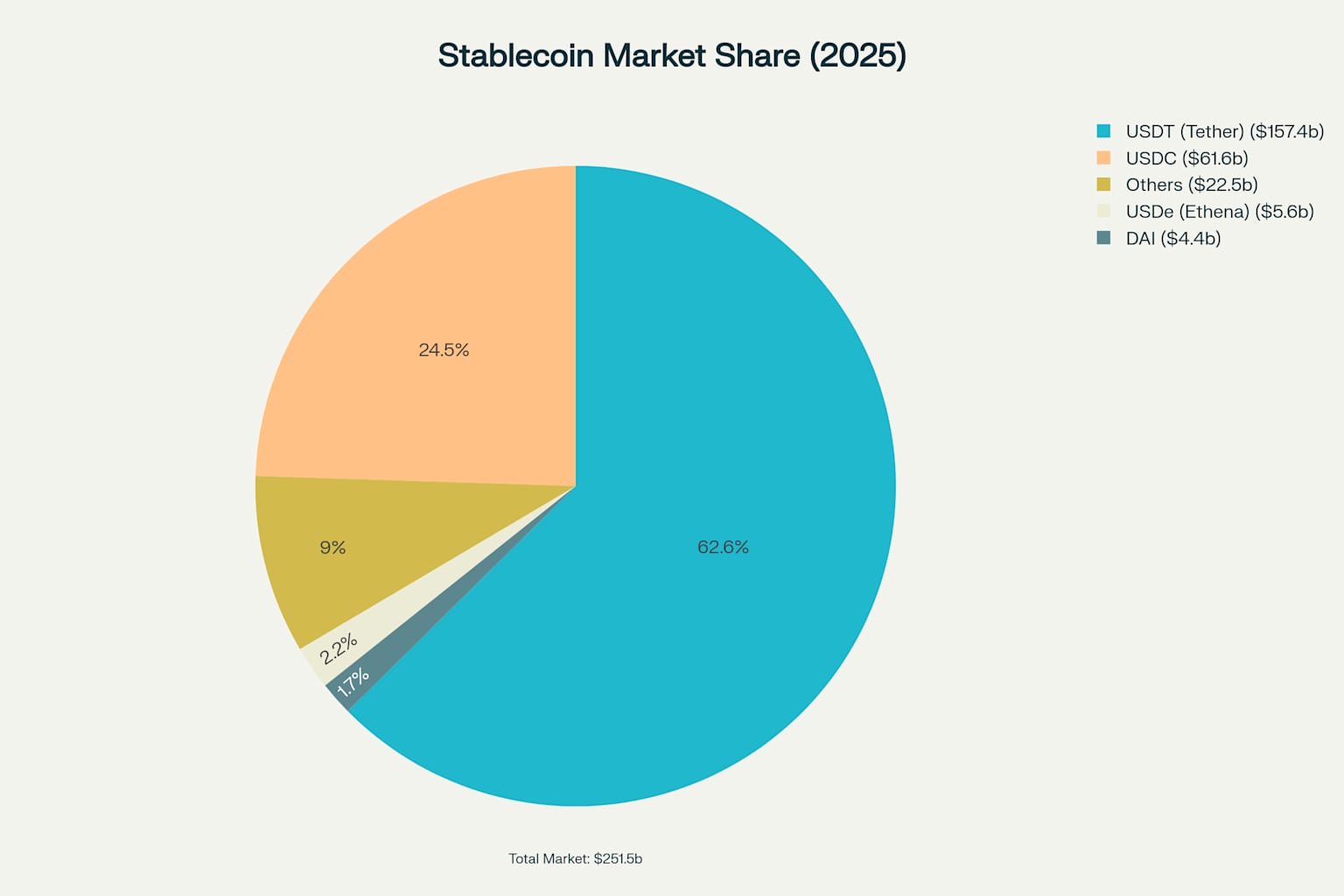

The stablecoin ecosystem demonstrates remarkable concentration, with Tether (USDT) commanding 62.6% market share at $157.4 billion in circulation, followed by USD Coin (USDC) at 24.5% with $61.6 billion outstanding. This duopoly controls 87.1% of the total market, creating systemic importance that regulators have identified as requiring federal oversight.

Transaction volume data reveals stablecoins’ transformative impact on global payments infrastructure. The $27.6 trillion processed in 2024 represents an 11.7% premium over traditional payment networks, positioning stablecoins as legitimate competitors to established financial rails. Stablecoin addresses have expanded to 121.67 million as of September 2024, with 19.70 million addresses actively transacting monthly.

Federal Reserve analysis indicates that stablecoin adoption patterns vary significantly by funding source and reserve composition. Cash inflows into stablecoins demonstrate neutral effects on credit provision, while commercial bank deposit substitution presents potential disruption risks depending on reserve frameworks. European research confirms that existing stablecoins already demonstrate critical importance to crypto-asset market liquidity.

Regulatory Framework Architecture

The GENIUS Act establishes three permitted issuer categories: subsidiaries of insured depository institutions, federal-qualified nonbank issuers regulated by the Office of the Comptroller of the Currency, and state-qualified issuers operating under substantially similar frameworks. The legislation implements a crucial $10 billion outstanding issuance threshold, requiring nonbank issuers above this limit to submit to federal oversight while permitting smaller operators to function under state regulation.

Reserve requirements mandate 1:1 backing with segregated liquid assets including U.S. dollars, short-term Treasuries with maturity of 93 days or less, overnight reverse repurchase agreements, and specified money market funds. The framework explicitly prohibits yield-bearing stablecoins, eliminating revenue models that compete with traditional deposit products.

Monthly disclosure requirements and anti-money laundering compliance create transparency standards exceeding current voluntary practices. Issuers with market capitalizations exceeding $50 billion must provide annual audited financial statements, while bankruptcy provisions ensure stablecoin holders receive priority claims on reserve assets.

Big Tech restrictions represent the most significant competitive barrier, requiring unanimous approval from the Treasury Secretary, Federal Reserve Chair, and FDIC Chair for public companies not predominantly engaged in financial activities. These provisions directly target potential stablecoin issuance by Amazon, Google, Apple, and Meta, while implementing strict data-use limitations prohibiting transaction data monetization.

Traditional Banking Response and Competitive Implications

Major U.S. banks have initiated early-stage discussions regarding joint stablecoin issuance, with companies linked to JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo exploring collaborative approaches. Early Warning Services, the parent company of digital payments network Zelle, and payment network Clearing House have joined these preliminary discussions.

The American Bankers Association’s position emphasizes that stablecoin regulation must not disrupt traditional credit creation mechanisms. Analysis indicates that financial inducements on stablecoins, such as PayPal’s proposed 3.7% reward on wallet balances, could incentivize value storage in payment stablecoins rather than bank deposits.

Federal Reserve research demonstrates that stablecoin impact on credit intermediation depends critically on funding sources and reserve composition. Narrow bank frameworks pose the greatest risk to credit provision when funded by commercial bank deposits, while two-tiered banking systems can support stablecoin issuance while maintaining traditional credit creation.

Banking sector concerns center on deposit disintermediation risks, regulatory compliance costs, and competition from non-bank issuers. However, potential benefits include new revenue streams, digital payment innovation, reduced settlement costs, and enhanced customer retention capabilities.

Implementation Timeline and Operational Challenges

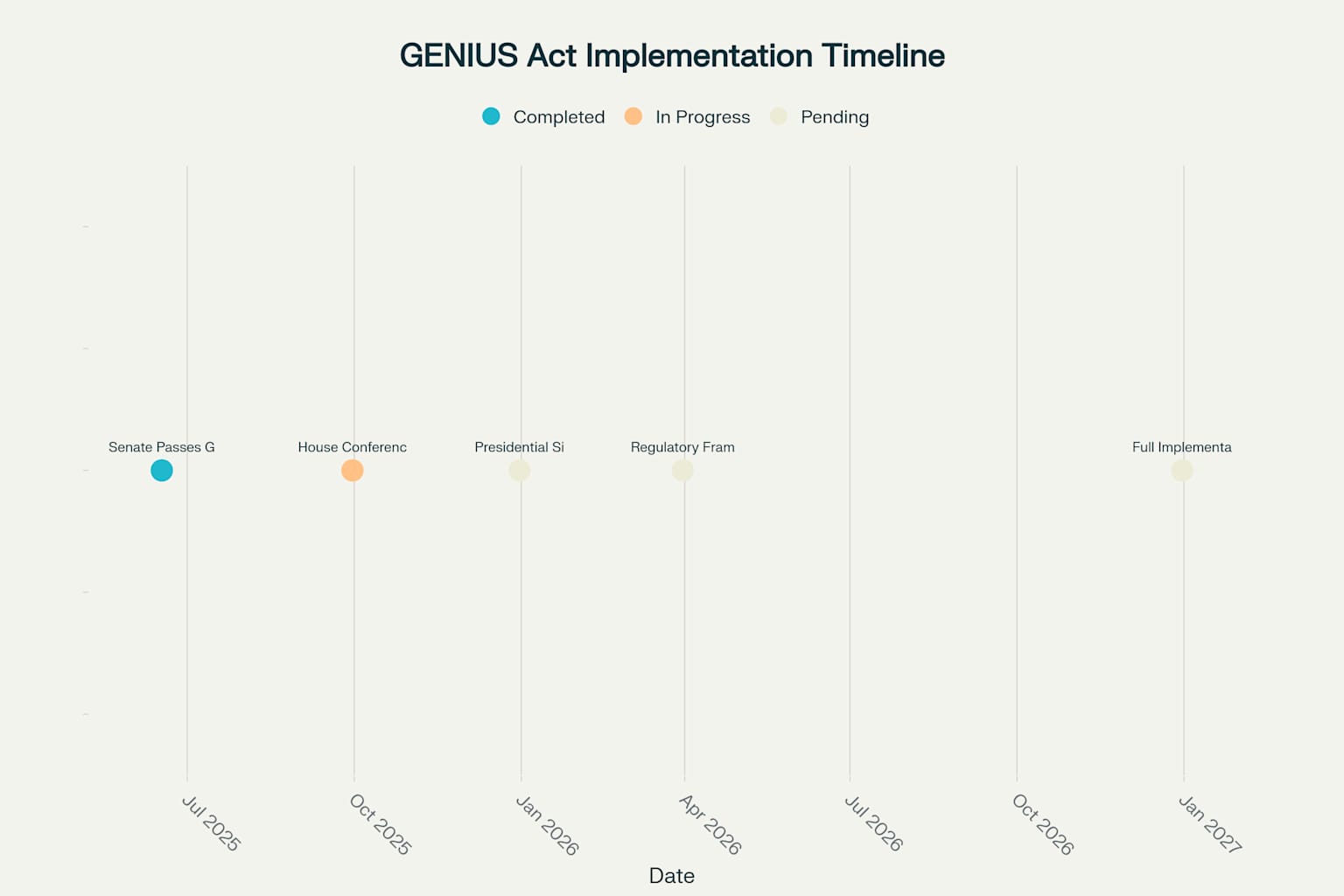

The GENIUS Act requires House reconciliation with the pending STABLE Act before presidential signature, with conferencing expected in Q3 2025 and enactment anticipated by Q4 2025. Federal regulators must act on issuer applications within 120-day windows, with 12-month safe harbor provisions for subsidiaries of insured depository institutions and federal-qualified issuers.

Implementation becomes operative within 18 months of enactment, with final rules potentially accelerating this timeline. The Treasury Department and OCC will establish licensing frameworks, operational standards, and examination procedures during the regulatory development phase.

Industry compliance preparation presents significant challenges, particularly for hybrid and algorithmic stablecoin models that fall outside the legislation’s scope. DeFi protocols utilizing stablecoins face uncertainty regarding regulatory treatment, with decentralized models like DAI requiring clear reserve accountability and issuer identification.

State regulatory frameworks must achieve “substantial similarity” to federal standards for smaller issuers, necessitating legislative action in many jurisdictions. The phase-in timeline requires existing issuers to demonstrate compliance or risk prohibition from U.S. operations.

International Regulatory Competition

The United States joins a growing cohort of jurisdictions implementing comprehensive stablecoin frameworks, including the United Kingdom, European Union, United Arab Emirates, and Hong Kong. The EU’s Markets in Crypto-Assets Regulation (MiCAR) provides a comparative framework with distinct approaches to reserve requirements and oversight structures.

Key differences between the GENIUS Act and MiCAR include more restrictive Big Tech provisions in U.S. legislation, faster implementation timelines, and explicit focus on maintaining U.S. dollar hegemony in digital assets. EU requirements mandate 30% of reserves at commercial banks for smaller stablecoins and 60% for significant issuers, contrasting with U.S. segregation requirements.

International financial authorities have issued warnings regarding stablecoin risks to monetary sovereignty, transparency concerns, and potential capital flight from developing nations. Some analysis draws parallels to 19th-century Free Banking period private banknotes, noting that stablecoins can trade at fluctuating exchange rates based on issuer credibility.

Treasury officials emphasize stablecoins as digital pillars of the dollar-based global financial system, positioning the GENIUS Act as strategic policy for maintaining reserve currency status. The legislation’s potential to reduce the impact of the $37 trillion U.S. debt load while strengthening dollar dominance represents significant geopolitical implications.

Market Structure and Competitive Dynamics

PayPal’s integration of PYUSD across its merchant network demonstrates corporate adoption strategies, with plans to offer stablecoin options for bill-pay products serving over 20 million small-to-medium enterprises. Meta and Walmart have announced exploratory initiatives for stablecoin payment integration, while Mastercard and Visa have developed blockchain settlement capabilities using USD Coin.

The prohibition on yield-bearing stablecoins eliminates competitive pressure on traditional deposit products while creating clearer regulatory boundaries. This restriction addresses concerns that interest-bearing stablecoins could accelerate deposit migration from traditional banks.

Algorithmic stablecoins face exclusion from the regulatory framework due to their failure to meet effective stabilization method requirements. Global standards require reserve-based stabilization methods with conservative, high-quality liquid assets, effectively eliminating purely algorithmic models.

Economic Impact Analysis

Stablecoin adoption patterns indicate significant cross-border payment utility, with use cases expanding beyond crypto trading to include remittances, corporate treasury management, and DeFi liquidity provision. The 15% increase in stablecoin-holding addresses throughout 2024 demonstrates growing mainstream adoption.

Federal Reserve analysis suggests that stablecoin inflows from cash-equivalent securities produce minimal credit provision impact, as funds recycle back into the banking system. However, deposit substitution scenarios present varying outcomes depending on reserve framework implementation.

The $2 trillion market projection represents a 695% growth rate from current levels, indicating potential systemic importance requiring coordinated regulatory oversight. This expansion would position stablecoins as significant components of the U.S. monetary system.

Conclusion

The GENIUS Act represents a watershed moment in digital asset regulation, establishing comprehensive federal oversight for a market segment that processes more transaction volume than traditional payment networks while maintaining the potential for exponential growth. The legislation’s bipartisan passage signals political recognition of stablecoins’ economic significance and strategic importance for maintaining U.S. dollar dominance in global digital finance.

Traditional banking institutions face fundamental strategic decisions regarding stablecoin participation, with early collaborative discussions indicating industry acknowledgment of competitive pressures. The regulatory framework’s tiered approach, Big Tech restrictions, and reserve requirements create a balanced structure that promotes innovation while maintaining financial stability safeguards.

Implementation success depends on effective House-Senate conferencing, coordinated regulatory agency action, industry compliance preparedness, and international regulatory coordination. The 18-month implementation timeline provides adequate adjustment periods while establishing clear competitive boundaries for market participants.

The GENIUS Act’s ultimate impact will be measured by its ability to foster responsible innovation, maintain banking system stability, and strengthen U.S. leadership in global digital finance architecture. As stablecoins evolve from experimental digital assets to regulated financial infrastructure, this legislation establishes the foundation for the next phase of monetary system evolution.