Spirit Airlines vs. DOT: Competition at a Crossroads

The U.S. airline industry stands at a critical juncture as Spirit Airlines challenges the Department of Transportation’s regulatory approach to airline partnerships, filing a formal appeal against the proposed JetBlue Airways-United Airlines “Blue Sky” alliance. This confrontation represents more than a single carrier’s grievance—it illuminates the fundamental tension between market consolidation and competition in an industry where the Big Four airlines already control nearly 70% of domestic market share.

Spirit’s challenge comes at a moment of unprecedented vulnerability for the ultra-low-cost carrier sector, with the airline having filed for Chapter 11 bankruptcy protection in November 2024 following years of mounting financial losses. The timing underscores the broader implications of airline partnerships for competitive dynamics, particularly as struggling carriers face an increasingly consolidated marketplace where strategic alliances between dominant players can reshape market access and pricing power.

The Evolving Landscape of Airline Market Concentration

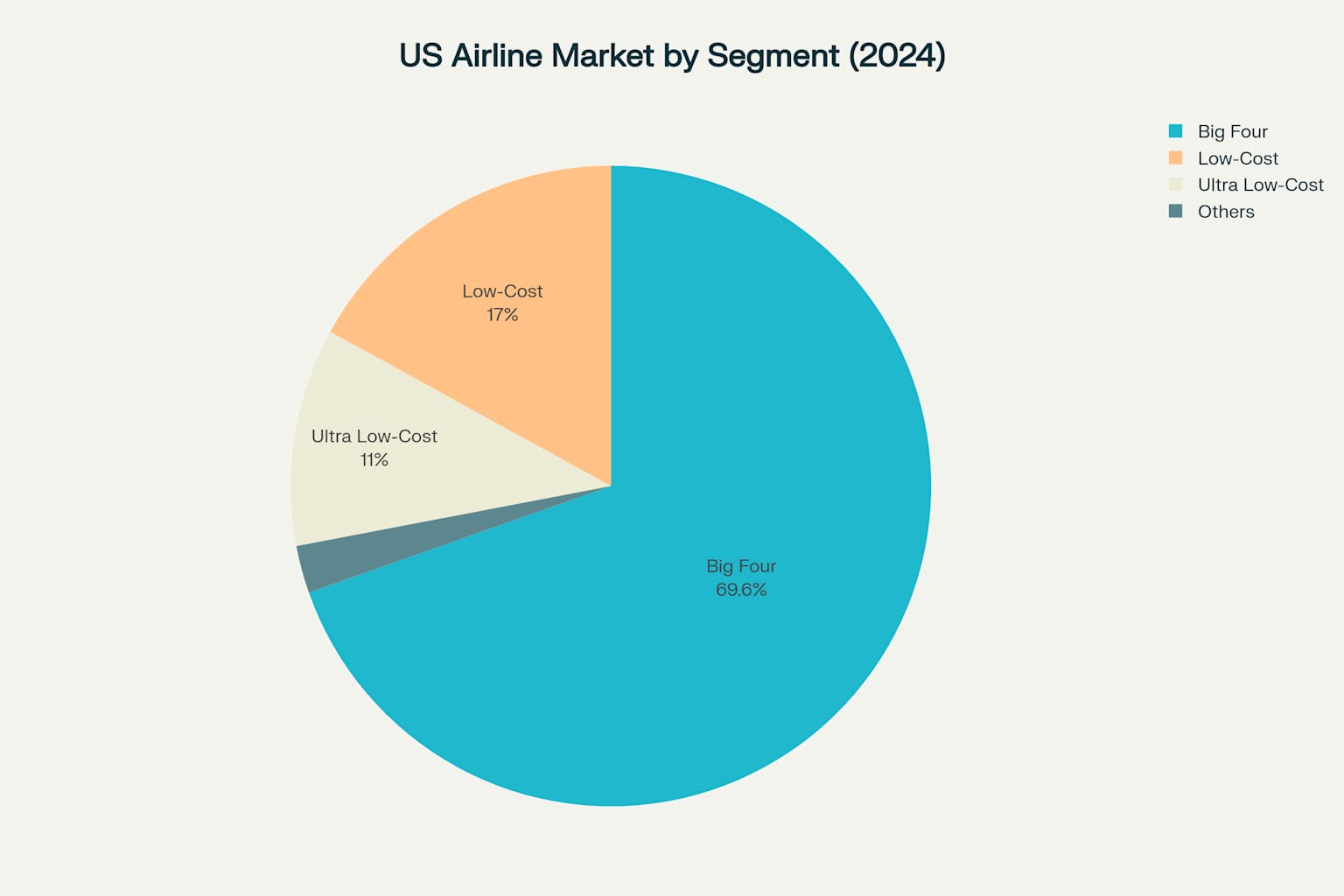

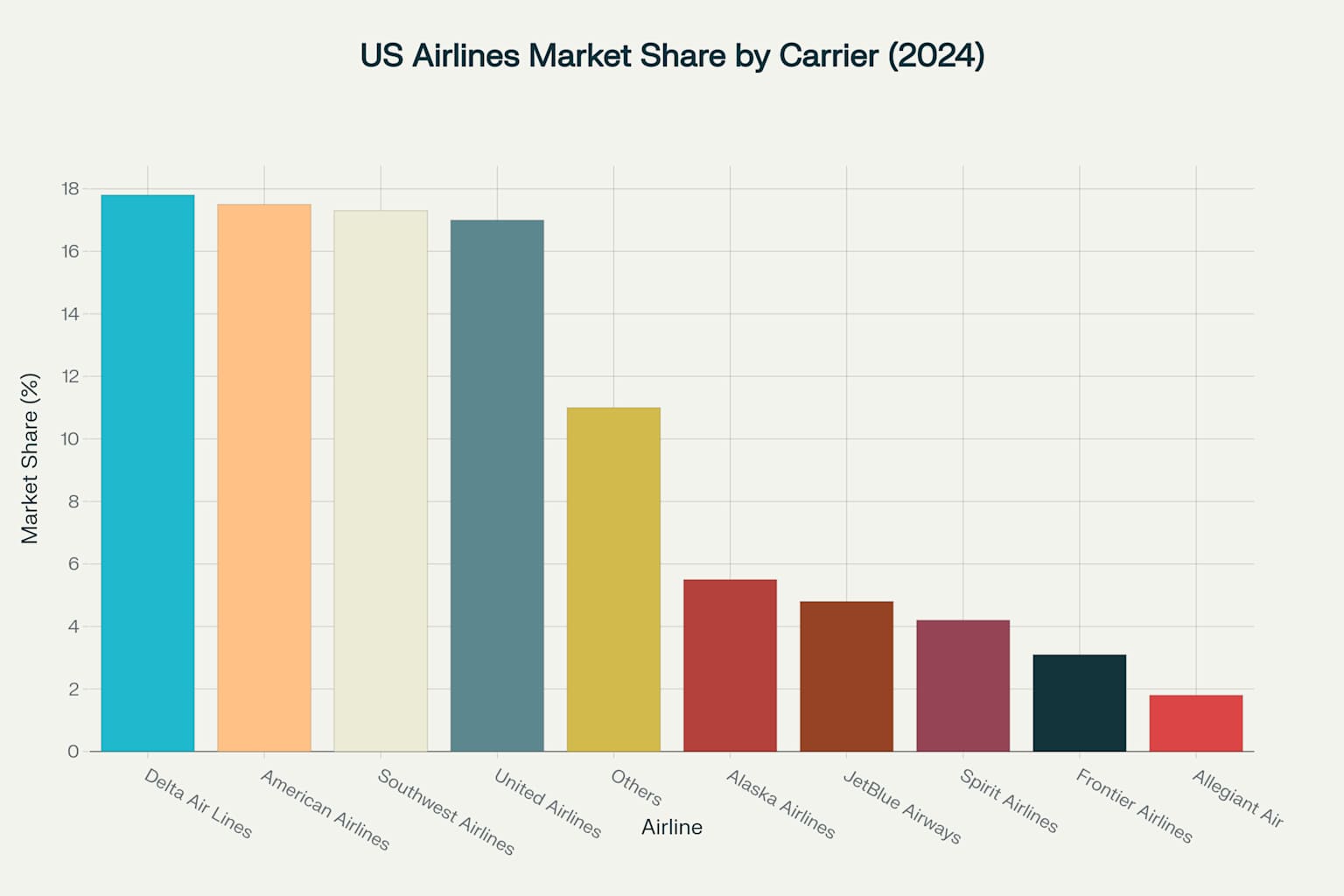

The U.S. airline industry has undergone dramatic consolidation over the past four decades, transforming from a landscape of dozens of competitors into one dominated by a handful of major carriers. Current market data reveals the extent of this concentration, with Delta Air Lines, American Airlines, Southwest Airlines, and United Airlines collectively commanding 69.6% of the domestic market.

Within this concentrated structure, ultra-low-cost carriers like Spirit occupy a precarious position, holding just 11% of total market share despite their role as price disciplinarians. Spirit Airlines specifically maintains a 4.2% market share, generating 37.09 billion revenue passenger miles annually, positioning it as the largest carrier within the ULCC segment.

The mathematical reality of market concentration becomes stark when examined through regulatory frameworks. Research demonstrates that ULCC presence in a market correlates with base fares 21% lower than average, compared to an 8% reduction for traditional low-cost carriers. However, this price discipline effect operates within increasingly constrained parameters as market concentration limits the number of routes where ULCCs can establish meaningful competition.

Spirit’s Financial Deterioration and Strategic Isolation

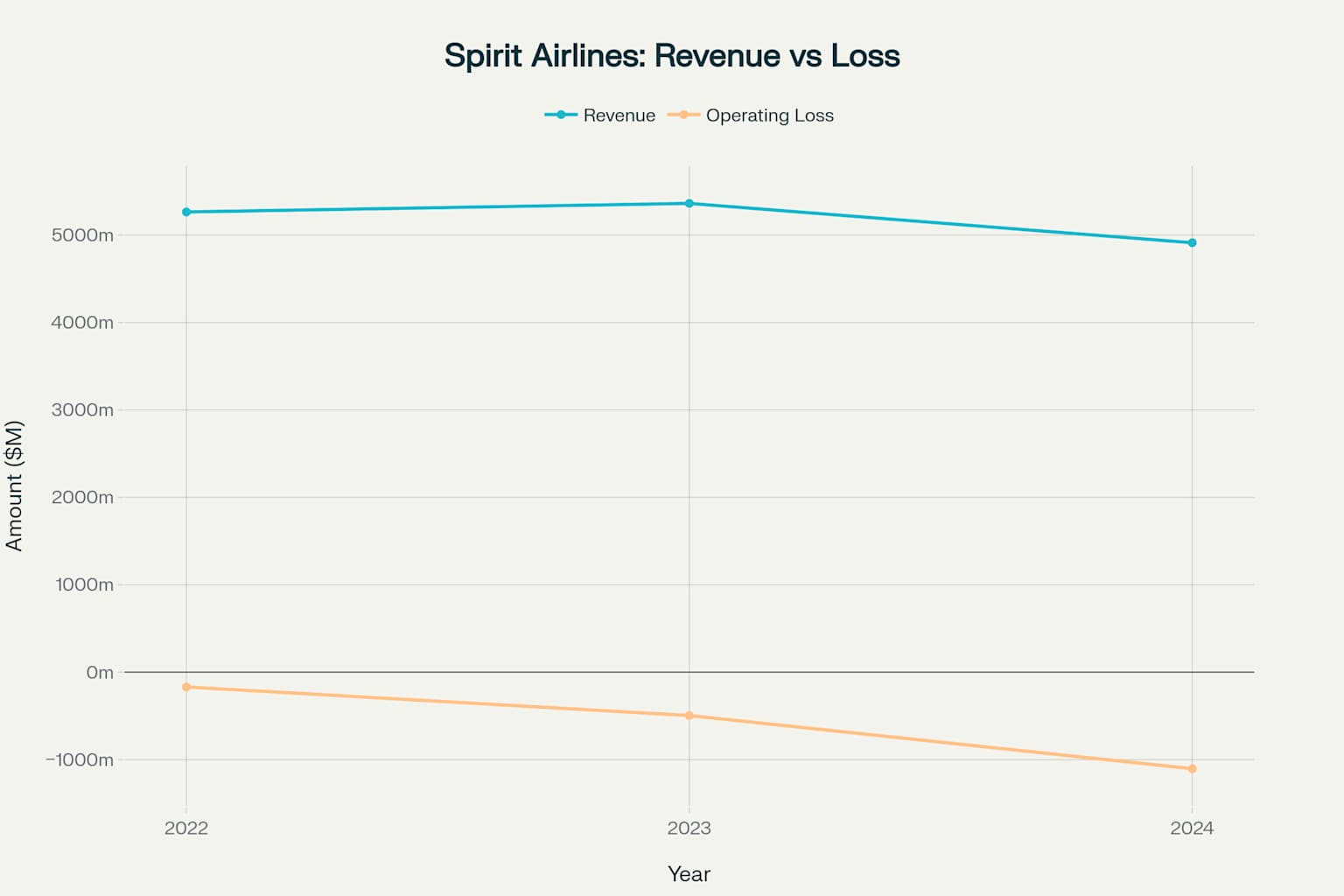

Spirit Airlines’ opposition to the Blue Sky partnership stems from a position of acute financial distress that has intensified dramatically over the past three years. Operating revenue declined from $5.265 billion in 2022 to $4.913 billion in 2024, while operating losses expanded from $169 million to $1.105 billion over the same period.

The carrier’s operating margin deteriorated to negative 22.5% in 2024, reflecting fundamental challenges in the ULCC business model amid industry headwinds. Revenue per passenger segment fell from $121.58 to $111.21, indicating pricing pressure that undermined the carrier’s core value proposition. These financial pressures culminated in Spirit’s Chapter 11 bankruptcy filing, occurring just months before the Blue Sky partnership announcement.

Source: simpleflying

Spirit’s strategic isolation became apparent following the federal court’s rejection of its proposed merger with JetBlue Airways in January 2024. The court ruled that eliminating Spirit would harm cost-conscious travelers who rely on the carrier’s low fares, effectively precluding consolidation opportunities for the struggling airline. This regulatory precedent creates a paradox where Spirit faces restrictions on merger activity while simultaneously confronting partnerships between larger carriers that may further constrain its competitive position.

The Blue-Sky Partnership: Structure and Competitive Implications

The JetBlue-United Blue Sky partnership, announced in May 2025, establishes a comprehensive alliance encompassing loyalty program integration, route coordination, and airport slot arrangements. The partnership allows customers to earn and redeem miles across both airlines’ networks while providing reciprocal elite benefits and streamlined booking capabilities.

Critical to the competitive analysis is the partnership’s impact on constrained airport markets, particularly John F. Kennedy International Airport where JetBlue will provide United access to up to seven daily round-trip flights beginning in 2027. United’s return to JFK represents a significant market development, as the carrier last operated from the airport in 2022. The slot arrangement effectively concentrates market power at one of the nation’s most capacity-constrained airports.

Spirit’s regulatory filing argues that the Blue Sky partnership mirrors the anticompetitive structure of the previously blocked Northeast Alliance between American Airlines and JetBlue. The carrier contends that loyalty program reciprocity creates economic dependencies that compromise JetBlue’s pricing independence, as the airline must purchase United miles to fulfill customer redemptions. These costs, Spirit argues, will be passed through to consumers in the form of higher fares.

DOT Regulatory Precedents and Partnership Assessment Framework

The Department of Transportation’s evaluation of airline partnerships operates within an established analytical framework that examines both competitive effects and consumer benefits. DOT’s precedent requires a two-step analysis: first determining whether partnership agreements adversely affect the public interest, then evaluating whether antitrust immunity grants serve the public interest.

Historical data from DOT partnership reviews indicates that fares for alliance itineraries average 25% lower than non-aligned interline itineraries, suggesting potential consumer benefits from coordination. However, these benefits must be weighed against potential anticompetitive effects, particularly in markets where partnership participants hold significant market positions.

The regulatory challenge lies in distinguishing between efficiency-enhancing coordination and market power consolidation. Academic research demonstrates that airline alliances can reduce double marginalization effects in connecting markets while potentially enabling coordinated pricing in overlapping routes. The Blue Sky partnership’s impact on these dynamics depends critically on the extent of route overlap and market concentration in affected city pairs.

Market Access and Slot Allocation Dynamics

Spirit’s challenge extends beyond the Blue Sky partnership to encompass broader issues of airport access and regulatory favoritism. The carrier’s unsuccessful applications for beyond-perimeter slots at Ronald Reagan Washington National Airport exemplify the challenges facing smaller carriers in accessing constrained infrastructure.

DOT’s October 2024 slot allocation awarded new beyond-perimeter exemptions to Alaska Airlines, American Airlines, Delta Air Lines, Southwest Airlines, and United Airlines while rejecting applications from Spirit, Frontier Airlines, and JetBlue Airways. Spirit challenged this decision through federal court, arguing that Alaska Airlines should have been disqualified due to its extensive codeshare relationship with American Airlines.

The slot allocation process reveals the self-reinforcing nature of market concentration, where established carriers’ existing market positions provide advantages in securing additional access rights. Spirit’s exclusion from new slot allocations constrains its ability to compete in key markets while incumbent carriers expand their networks.

Implications for ULCC Business Model Viability

The confrontation between Spirit and DOT illuminates fundamental questions about the long-term viability of the ultra-low-cost carrier business model within an increasingly consolidated industry structure. ULCC market share has grown from 6% to 11% over the past decade, primarily at the expense of traditional full-service carriers. However, this growth occurred during a period of relative industry stability that may not persist.

Research indicates that ULCCs demonstrate higher volatility than legacy carriers, with Spirit and similar operators three times more likely to abandon markets within two years of entry compared to traditional low-cost carriers. This operational instability undermines the competitive discipline that ULCCs provide to incumbent carriers, potentially reducing long-term consumer benefits from their market presence.

The financial pressures facing Spirit reflect broader challenges within the ULCC segment, where operational disruptions disproportionately impact margins compared to legacy carriers. Industry consolidation through partnerships like Blue Sky may exacerbate these pressures by reducing access to connecting traffic and constrained airport facilities.

Regulatory Response and Industry Evolution

DOT’s handling of the Blue Sky partnership will establish important precedents for future airline cooperation arrangements. Spirit’s appeal specifically requests extended review periods and public comment opportunities, arguing that regulatory transparency should match the scrutiny applied to formal mergers. The carrier’s position reflects broader concerns about regulatory consistency in addressing different forms of industry consolidation.

The International Air Transport Association projects global airline industry revenues will exceed $1 trillion in 2025, with North American carriers contributing significantly to this growth. However, profit margins remain constrained at approximately 3.6% industry-wide, reflecting ongoing competitive pressures despite market concentration. These financial realities create incentives for further consolidation through partnerships that may skirt traditional merger review processes.

Current capacity growth projections show modest 1-2% increases across major U.S. markets, suggesting limited opportunities for new entrant expansion. Supply chain constraints and aircraft delivery delays further limit competitive entry, potentially strengthening the market position of established partnerships like Blue Sky.

Conclusion

Spirit Airlines’ challenge to the JetBlue-United Blue Sky partnership represents a defining moment for competition policy in the U.S. airline industry. The confrontation exposes fundamental tensions between regulatory approaches to formal mergers versus strategic partnerships, highlighting gaps in competitive oversight that may enable market concentration through alternative mechanisms.

The financial collapse of Spirit Airlines—from industry disruptor to bankruptcy protection—demonstrates the vulnerability of competitive alternatives within highly consolidated markets. DOT’s response to Spirit’s appeal will signal whether regulatory authorities recognize partnership arrangements as potential substitutes for traditional merger activity requiring equivalent scrutiny.

For consumers, the outcome carries implications extending beyond airline choice to fundamental questions about market structure and pricing discipline. The data indicates that ULCC presence reduces market fares by 21%, making the preservation of competitive alternatives a significant consumer welfare issue. However, the financial sustainability of these alternatives remains questionable absent regulatory intervention to preserve market access and prevent coordination among dominant carriers.

The broader industry trajectory toward increased concentration through partnerships rather than mergers may require updated regulatory frameworks that recognize the competitive effects of strategic alliances. As the Blue Sky partnership moves toward implementation, the airline industry watches whether DOT will address Spirit’s concerns or allow market forces to continue their consolidation trajectory through alternative mechanisms.