Oil Prices Tumble: From Middle East Calm to Energy Sector Slump

The recent resolution of the Israel-Iran conflict has triggered a dramatic reversal in global oil markets, with crude prices plummeting nearly 15% from their June peak as geopolitical tensions subsided and supply disruption fears evaporated. This sharp decline from Brent crude’s high of $81.40 per barrel to $67.20 represents more than a typical market correction—it demonstrates the profound impact of geopolitical risk premiums on energy markets and reveals the cascading effects across producers, consumers, and financial markets.

The magnitude of this price movement extends far beyond the 5% threshold typically associated with significant market shifts, instead delivering a comprehensive realignment of economic expectations across the energy sector. Analysis of the underlying market dynamics reveals how supply and demand elasticities interact with geopolitical shocks to produce outsized price volatility, while simultaneously redistributing economic benefits and costs across the global economy.

The Geopolitical Catalyst and Market Response

Middle East Tensions Drive Initial Price Surge

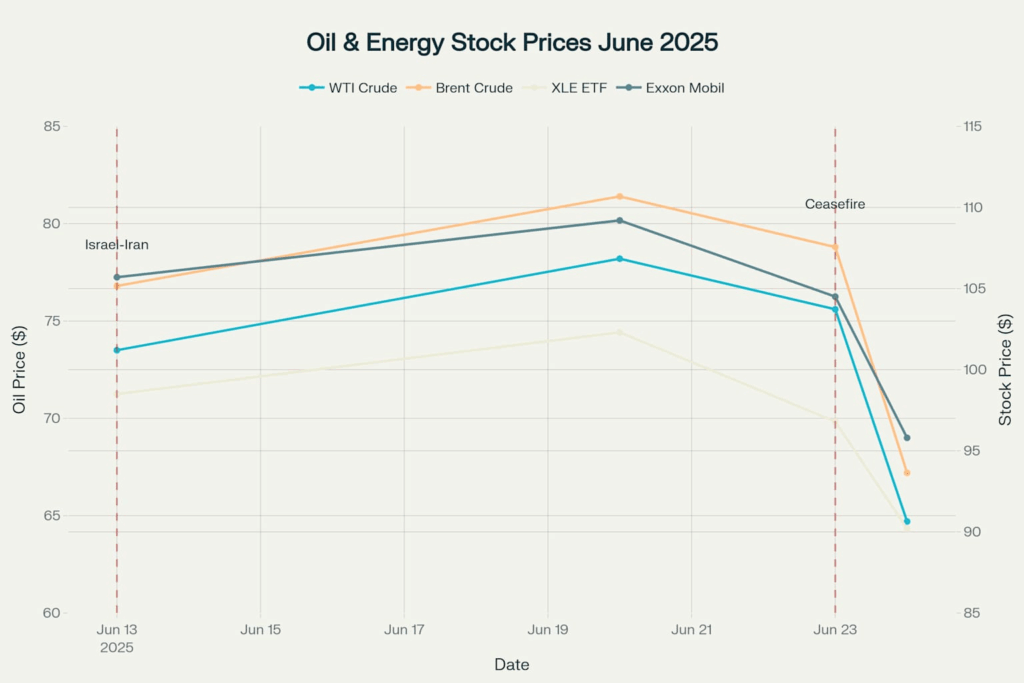

The crisis began on June 13, 2025, when Israel launched unprecedented strikes against Iranian nuclear facilities, immediately raising concerns about potential disruptions to the Strait of Hormuz, through which approximately 21 million barrels per day—representing 20% of global oil supply—transits daily. Within days, Brent crude prices surged from pre-crisis levels of $76.80 per barrel to a five-month high of $81.40, while West Texas Intermediate climbed from $73.50 to $78.20.

Energy markets responded with characteristic volatility to supply disruption fears, as traders priced in the potential for Iran to retaliate by blocking the strategic waterway. The rapid price escalation demonstrated the sensitivity of oil markets to Middle Eastern geopolitical developments, particularly those involving critical transportation chokepoints.

Ceasefire Announcement Triggers Sharp Reversal

The announcement of a ceasefire between Israel and Iran on June 23-24 precipitated an immediate and dramatic market reversal. Oil prices fell nearly 6% in a single trading session, with both Brent and WTI crude dropping below pre-crisis levels. This swift decline eliminated the geopolitical risk premium that had accumulated during the conflict, returning prices to levels last seen before the hostilities began.

The speed and magnitude of the price collapse highlighted the significant risk premium embedded in oil markets during the crisis period. Market participants had priced in scenarios ranging from temporary supply disruptions to potential closure of the Strait of Hormuz, creating substantial downside momentum once these risks dissipated.

Quantitative Analysis of Market Dynamics

Supply and Demand Elasticity Framework

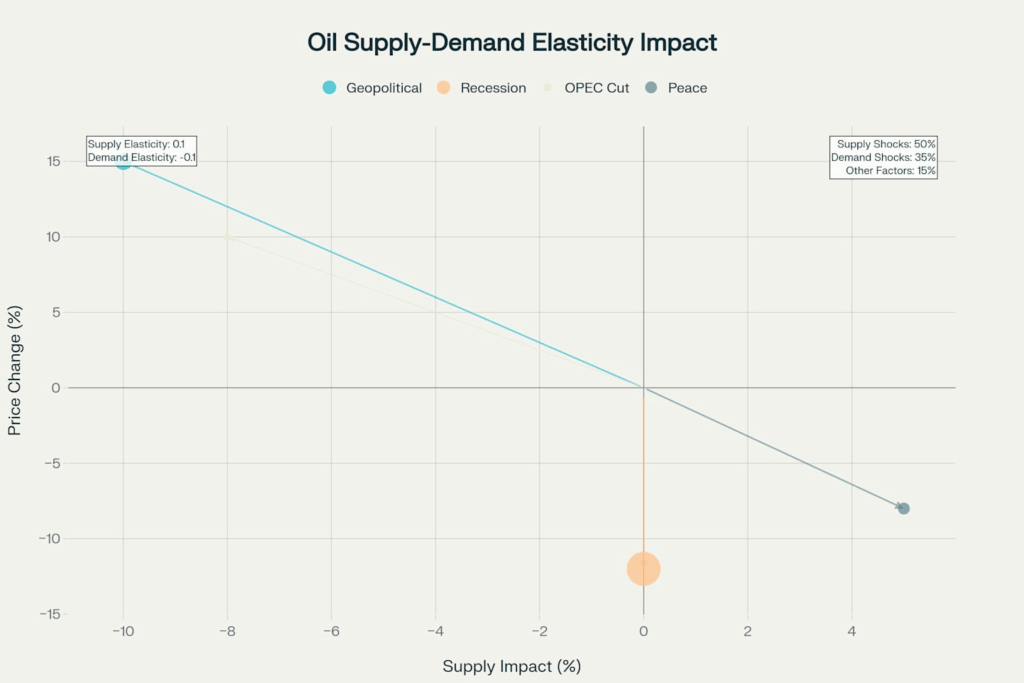

Economic modeling reveals that oil market price movements are governed by specific elasticity parameters that determine how supply and demand respond to price changes. Federal Reserve research indicates short-run oil supply elasticity of approximately 0.1 and oil demand elasticity of -0.1, meaning both supply and demand respond relatively inelastically to price changes in the short term.

This elasticity framework explains why geopolitical shocks produce such pronounced price volatility. With supply and demand curves that are relatively steep, even modest shifts in either schedule generate significant price movements. Analysis shows that supply shocks account for approximately 50% of oil price fluctuations, while demand shocks contribute 35%, with the remainder attributed to other factors including geopolitical risk premiums.

Price Shock Decomposition

The recent oil price decline can be decomposed into its constituent elements using structural vector autoregression models. The elimination of geopolitical risk premiums represents a supply-side shock, as markets reassess the probability of production disruptions. Simultaneously, concerns about global economic growth amid trade tensions contribute demand-side pressure.

International Energy Agency forecasts indicate global oil demand growth of only 720,000 barrels per day in 2025, down from previous estimates and representing the third consecutive year of sub-1 million barrel daily growth. This sluggish demand trajectory, combined with OPEC+ production increases, creates fundamental oversupply conditions that amplify price declines when risk premiums dissipate.

Impact on Oil Producers and Energy Companies

Upstream Producer Revenue Compression

Oil producers face immediate and substantial revenue impacts from the price decline. For upstream companies engaged in exploration and production, the drop from peak prices of approximately $81 to current levels near $67 represents a revenue reduction of roughly 17%. This compression occurs instantaneously as oil sales are typically priced at prevailing market rates, while production costs remain largely fixed in the short term.

First-quarter 2025 earnings data demonstrates the sensitivity of producer profitability to oil price movements. A group of 41 US-based oil and gas producers reported combined net income of $19.83 billion, down from $26.39 billion in the previous year, reflecting the impact of lower average oil prices. Brent crude averaged $75.81 per barrel in the first quarter compared to $83.00 in the prior year period.

Downstream Refining Sector Mixed Impact

Oil refiners experience more complex dynamics during price declines. While lower crude oil input costs provide some relief, refining margins often compress simultaneously as product prices decline alongside crude. The relationship between crude costs and refined product prices varies by region and product mix, creating asymmetric impacts across different refining configurations.

Refinery utilization rates demonstrate the operational challenges facing the downstream sector. US refinery utilization stood at 86.9% in the first quarter of 2025, compared to 85.8% in the prior year, but below the 91.6% rate achieved in the fourth quarter of 2024. This declining trend reflects both seasonal maintenance patterns and margin pressures that discourage maximum throughput operations.

Geographic and Operational Variations

The impact of oil price declines varies significantly by producer location and operational characteristics. US shale oil producers, which generally require higher breakeven prices than conventional operations, face particular pressure from sustained price weakness. Recent analysis indicates that current oil prices have fallen below the level where US producers can profitably drill new wells on average.

Oil-exporting nations experience immediate fiscal pressure from reduced export revenues. Countries with high fiscal breakeven oil prices face particular challenges in maintaining government spending and economic stability when prices decline significantly. The impact extends beyond direct government revenues to affect employment, investment, and broader economic activity in oil-dependent regions.

Energy Sector Stock Performance and Financial Markets Impact

Immediate Equity Market Response

Energy sector stocks experienced severe declines following the oil price collapse, with the Energy Select Sector SPDR ETF (XLE) falling 16% over two trading days. This amplified response reflects the leveraged nature of equity valuations to underlying commodity prices, as fixed costs magnify the impact of revenue changes on profit margins.

Individual energy company performance varied based on operational profiles and financial leverage. ExxonMobil, despite being one of the largest integrated oil companies, declined 11.8% since the tariff and oil price decline announcement, demonstrating relatively resilient performance compared to more specialized producers. Smaller exploration and production companies faced more severe declines, with some falling over 20% during the same period.

Sectoral Performance Divergence

The oil price decline created clear winners and losers across different equity sectors. While energy companies faced significant pressure, transportation, manufacturing, and consumer-focused industries benefited from reduced input costs. Airlines, in particular, stand to benefit substantially from lower fuel costs, though the full impact typically takes time to materialize in fare reductions.

The Philadelphia Oil Service Sector Index declined 4.4%, reflecting the impact on companies providing services to energy producers. This decline demonstrates how oil price weakness cascades through the entire energy value chain, affecting not just producers but also equipment suppliers, drilling contractors, and technical service providers.

Valuation Adjustments and Fair Value Estimates

Investment analysts have adjusted fair value estimates for energy companies downward in response to the price decline. Morningstar reduced fair value estimates for shale oil stocks by up to 4%, reflecting the lower expected cash flows from reduced oil prices. Despite these reductions, several companies continue trading below revised fair value estimates, suggesting potential value opportunities for investors willing to accept commodity price volatility.

Devon Energy trades at $29.53, down 23% since the oil price decline began, compared to its lowered fair value estimate of $48 per share. Similarly, Diamondback Energy declined 23.7% to $125 per share against a revised fair value of $165, while Occidental Petroleum fell 17.9% to just over $40 per share compared to its $60 fair value.

Consumer and Economic Implications

Gasoline Price Relief

The oil price decline translates directly into consumer savings at the gasoline pump, though with typical lags as refined product prices adjust to crude oil changes. Current gasoline prices average approximately $3.12 per gallon nationally, with analysts forecasting potential declines below $3.00 during the summer driving season as the oil price reduction works through the system.

Consumer spending analysis indicates that roughly 80% of savings from lower gasoline prices are redirected to other economic activities. JPMorgan estimates that a dollar swing in gasoline prices translates to tens of billions of dollars in consumer purchasing power annually, providing significant economic stimulus when prices decline.

Manufacturing and Transportation Benefits

Lower oil prices provide immediate cost relief across multiple economic sectors. Transportation companies benefit from reduced fuel costs and the elimination of fuel surcharges, while manufacturers experience lower input costs for petroleum-based materials and reduced transportation expenses.

Source: energyeducation

The chemical industry receives particular benefits from lower oil prices, as petroleum serves as both an energy source and a feedstock for petrochemical production. This dual impact creates compound cost savings that can improve profit margins substantially during periods of sustained lower oil prices.

Macroeconomic Growth Implications

The oil price decline functions as an effective economic stimulus, particularly for oil-importing nations. Economic analysis suggests that sustained lower oil prices can add approximately 1% to economic growth over a five-year period, though current projections are tempered by concurrent trade tensions and global economic uncertainty.

However, the net economic impact varies significantly by country and economic structure. Oil-exporting nations face offsetting negative effects from reduced export revenues, while the global impact depends on the relative magnitude of benefits to oil importers versus costs to exporters.

Supply-Demand Fundamentals and Market Outlook

Global Demand Trajectory

Oil demand growth continues to decelerate amid economic headwinds and the gradual adoption of alternative energy technologies. The International Energy Agency projects global oil demand will increase by only 720,000 barrels per day in 2025, representing a significant slowdown from historical averages. This growth rate reflects continued expansion in developing economies, particularly India and other Asian markets, offset by declining consumption in developed nations.

Long-term demand projections indicate peak oil consumption may occur by 2029, followed by a gradual decline as electric vehicle adoption accelerates and energy efficiency improvements reduce petroleum requirements. However, these forecasts remain subject to significant uncertainty regarding the pace of technological adoption and economic development patterns.

Production Capacity and OPEC+ Response

Global oil production capacity continues expanding despite recent price weakness. OPEC+ members have begun unwinding production cuts implemented during previous market downturns, adding approximately 330,000 barrels per day to global supply in recent months. Current OPEC crude oil production stands at 29.0 million barrels per day, up 1.17% from the previous year.

The production increase comes at a time when demand growth remains constrained, creating fundamental oversupply conditions that pressure prices beyond the geopolitical factors. Saudi Arabia’s apparent shift away from supporting oil prices through production cuts suggests a new market dynamic where price volatility may be tolerated in favor of market share preservation.

Inventory Dynamics and Strategic Reserves

Global oil inventories have been building in recent months, providing additional downward pressure on prices. Commercial crude oil stocks in the United States totaled 431 million barrels at the end of March 2025, below year-earlier levels but reflecting seasonal patterns and refinery maintenance activities.

The availability of strategic petroleum reserves provides additional market stability, with the International Energy Agency maintaining 1.2 billion barrels in emergency stockpiles that can be deployed if supply disruptions materialize. This reserve capacity helps explain why markets quickly eliminated risk premiums once the immediate geopolitical threat subsided.

Conclusion

The dramatic oil price decline from Middle East tensions to ceasefire resolution demonstrates the powerful influence of geopolitical risk premiums on energy markets and their rapid dissipation when threats recede. The approximately 15% price drop from peak to trough represents more than a simple market correction—it reflects a fundamental reassessment of supply disruption risks and underlying market fundamentals.

The economic implications extend far beyond the energy sector itself, creating clear winners and losers across the global economy. Oil producers and energy sector investors face immediate revenue and valuation pressures, while consumers, transportation companies, and manufacturers benefit from reduced input costs. The magnitude and speed of these impacts underscore the continued central role of petroleum in the global economy despite ongoing energy transition efforts.

Looking forward, the convergence of weakening demand growth, expanding production capacity, and reduced geopolitical risk premiums suggests oil markets may remain under pressure in the near term. However, the inherent volatility of energy markets, combined with ongoing geopolitical uncertainties and the gradual nature of energy transitions, ensures that price dynamics will continue evolving in response to changing fundamentals and external shocks.

The recent episode serves as a reminder that while markets efficiently price known risks, the resolution of those risks can produce equally dramatic reversals that redistribute economic benefits across sectors and regions. For policymakers, investors, and businesses, the challenge remains navigating this volatility while positioning for the longer-term structural changes reshaping global energy markets.