India’s Currency Comeback: How Oil’s Drop Fueled the Rupee Rally

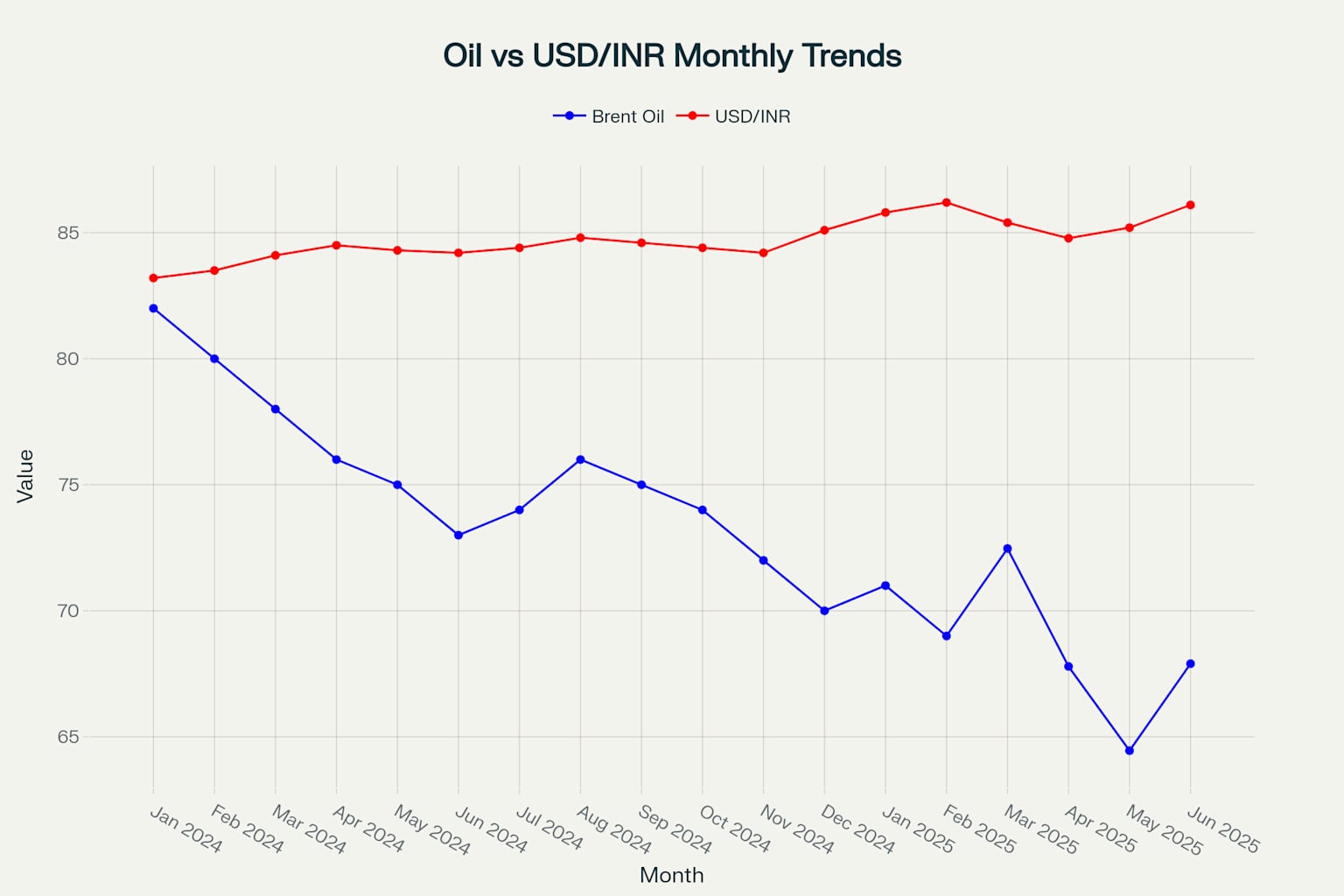

The Indian rupee has experienced a remarkable transformation over the past 18 months, with its performance closely tied to the dramatic decline in global crude oil prices. As Brent crude tumbled from over $82 per barrel in January 2024 to recent lows of $64.45 in May 2025, the rupee strengthened substantially, demonstrating one of the most significant correlations between commodity prices and currency movements in emerging markets. This relationship has profound implications for India’s economic stability, given that the country imports approximately 88% of its crude oil requirements and spent $137 billion on oil imports in fiscal year 2025.

The Mechanics of the Oil-Rupee Correlation

Quantifying the Inverse Relationship

The statistical relationship between oil prices and the rupee exchange rate reveals a robust negative correlation coefficient of -0.776, indicating that as oil prices decline, the rupee tends to strengthen against the US dollar. This inverse correlation operates through multiple transmission channels that directly impact India’s external sector balance.

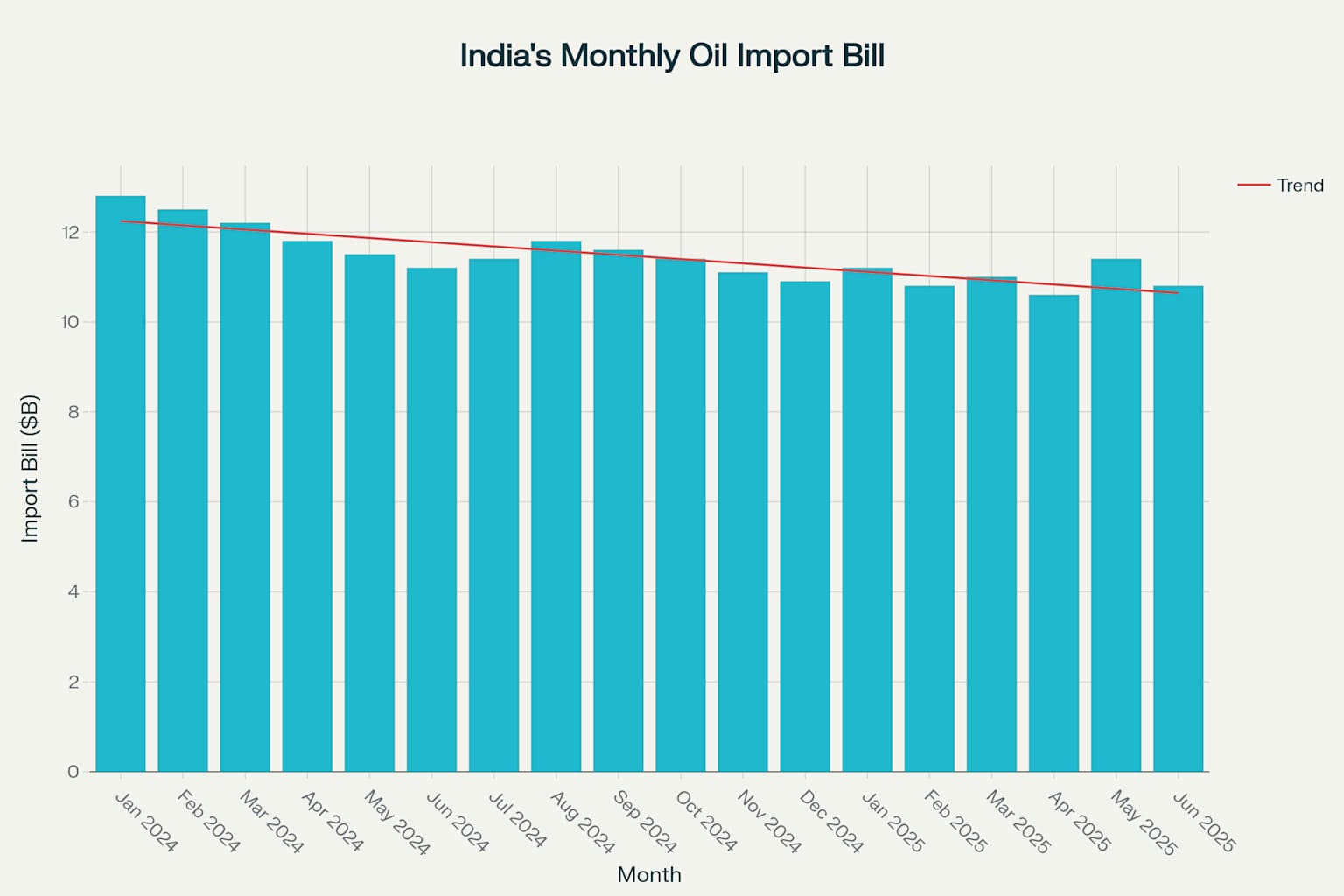

Data analysis spanning January 2024 to June 2025 demonstrates this relationship clearly: when Brent crude prices fell from $82 to $64.45 per barrel, representing a 17.2% decline, India’s monthly oil import bill decreased from $12.8 billion to $10.8 billion, a reduction of 15.6%. The rupee responded by strengthening from levels around 83.2 against the dollar to periodic lows of 84.78, before recent volatility pushed it back toward 86.1 levels.

Import Bill Dynamics and Currency Impact

India’s massive energy import dependency creates a direct transmission mechanism between global oil prices and rupee performance. The country’s crude oil import bill rose 2.7% to $137 billion in fiscal year 2025, despite a 17% decline in oil prices, due to increased volumes that totaled 234.3 million tonnes. However, monthly variations show the immediate impact of price changes on the trade balance and currency dynamics.

Research by Union Bank of India quantifies this sensitivity: every $10 per barrel increase in oil prices widens India’s current account deficit by approximately $15 billion annually. Conversely, the recent oil price decline has provided substantial relief to India’s external balances, with the current account deficit projected at 0.9% of GDP for fiscal year 2025, down from previous estimates.

Central Bank Policy Response and Market Dynamics

Reserve Bank of India’s Monetary Accommodation

The Reserve Bank of India has capitalized on the favorable external environment created by lower oil prices to implement aggressive monetary easing. Since February 2025, the RBI has cut the repo rate by a cumulative 100 basis points, bringing it down from 6.5% to 5.5% in three consecutive moves of 25, 25, and 50 basis points respectively.

This monetary policy stance shift from “accommodative” to “neutral” reflects the central bank’s assessment that inflation pressures have eased sufficiently to support growth. Headline consumer price inflation moderated to a nearly six-year low of 3.2% in April 2025, well below the RBI’s 4% target, providing room for continued policy support.

Foreign Portfolio Investment Flows

The improved macroeconomic backdrop has attracted significant foreign portfolio investment inflows. Foreign investors pumped ₹19,860 crore into Indian equities in May 2025, marking the highest monthly inflow for the year and the second consecutive month of net inflows. This represents a reversal from earlier outflows totaling ₹116,574 crore in the first quarter of 2025.

Global Supply Chain and Geopolitical Factors

Middle East Tensions and Oil Market Volatility

Recent geopolitical developments in the Middle East have tested the oil-rupee correlation. The Israel-Iran conflict in June 2025 initially pushed Brent crude prices above $80 per barrel, triggering concerns about supply disruptions through the Strait of Hormuz. However, the subsequent ceasefire agreement and de-escalation led to a sharp reversal, with oil prices falling over 15% in two sessions to settle near $67-68 per barrel.

The rupee’s response to these oil price movements was immediate and pronounced, weakening to 86.86 per dollar during the initial oil spike before recovering to 86.1 as tensions eased. This episode reinforced the sensitivity of the Indian currency to oil market developments and highlighted the ongoing risks from geopolitical instability.

Import Diversification and Supply Security

India’s oil import portfolio reflects strategic diversification efforts aimed at ensuring supply security while capturing price advantages. Russia emerged as India’s largest oil supplier in 2024, accounting for $45.4 billion of imports, followed by Iraq at $28.5 billion and Saudi Arabia at $23.5 billion.

The shift toward Russian crude, which trades at a $3-8 per barrel discount to other grades, has provided additional savings for Indian refiners. US crude imports also surged to 289,000 barrels per day in March 2025, up from 113,000 barrels per day a year earlier, as refiners sought supply diversification.

Structural Economic Implications

Current Account Dynamics and External Stability

The relationship between oil prices and India’s external accounts extends beyond immediate import costs to broader structural implications. India’s oil import dependency reached 88.2% in fiscal year 2025, up from 87.8% in the previous year, reflecting continued growth in domestic consumption despite stagnant domestic production.

Source: jmbaxi

This increasing dependence amplifies the economy’s sensitivity to global oil price movements. MUFG Bank estimates that with every $10 per barrel increase in oil prices, India’s current account deficit rises by 0.4% of GDP. The current environment of lower oil prices has therefore provided crucial breathing room for India’s external balances.

Inflation Transmission and Monetary Policy Space

Lower oil prices have created favorable conditions for inflation management, enabling the RBI to pursue growth-supportive policies. The direct impact on transportation and energy costs, combined with reduced import bill pressures on the exchange rate, has helped keep core inflation contained. This has allowed policymakers to focus on supporting economic growth, which is projected at 6.5% for fiscal year 2026.

Future Outlook and Potential Headwinds

Structural Vulnerabilities and Risk Factors

Despite the current favorable environment, several structural factors pose ongoing risks to the oil-rupee relationship. India’s continued dependence on energy imports leaves the economy vulnerable to sudden oil price spikes, particularly those driven by geopolitical events. The recent Middle East tensions demonstrated how quickly market conditions can change.

Climate transition policies and global decarbonization efforts may introduce new variables into traditional oil market dynamics. Additionally, potential changes in US trade policy and tariff structures present additional uncertainties for Indian external trade.

Central Bank Intervention Capacity

The RBI’s approach to currency management has evolved to focus on preventing excessive volatility rather than defending specific levels. Governor Sanjay Malhotra has indicated tolerance for gradual rupee depreciation, provided it remains orderly. However, the central bank maintains readiness to intervene if oil price shocks threaten financial stability.

India’s foreign exchange reserves of approximately $705 billion provide substantial firepower for such interventions. These reserves, equivalent to over 11 months of imports, offer a crucial buffer against external shocks.

Conclusion

The relationship between falling oil prices and rupee performance represents one of the most significant macroeconomic developments for India in recent years. The 17% decline in oil prices has delivered substantial benefits through reduced import costs, improved current account dynamics, and enhanced monetary policy flexibility. This has enabled the RBI to implement aggressive rate cuts totaling 100 basis points while maintaining price stability.

However, the sustainability of this favorable environment depends on continued stability in global oil markets and effective management of India’s structural energy dependencies. The recent geopolitical volatility serves as a reminder that oil price dynamics can shift rapidly, potentially reversing the currency gains achieved over the past 18 months. Policymakers must therefore use this period of relative stability to strengthen economic fundamentals and reduce vulnerabilities to external energy shocks.

The oil-rupee correlation will likely remain a critical factor in India’s economic outlook, making careful monitoring of global energy markets essential for maintaining macroeconomic stability and supporting the country’s growth trajectory.