Fed’s Rate Cut Gamble: Why Lowering Rates Amid Tariff Wars Will Backfire

The Federal Reserve’s consideration of rate cuts while tariffs create inflationary pressure represents a dangerous policy contradiction that will either fuel inflation or prove ineffective against economic headwinds, revealing the Fed’s policy toolkit is inadequate for the current economic reality. Chair Jerome Powell’s testimony before Congress this week exposed the central bank’s policy incoherence: admitting that Fed projections are for inflation to move up because of tariffs while simultaneously signaling potential rate cuts later this year. This represents perhaps the most reckless monetary policy gamble since the stagflationary disasters of the 1970s.

The Data Reveals an Unprecedented Policy Contradiction

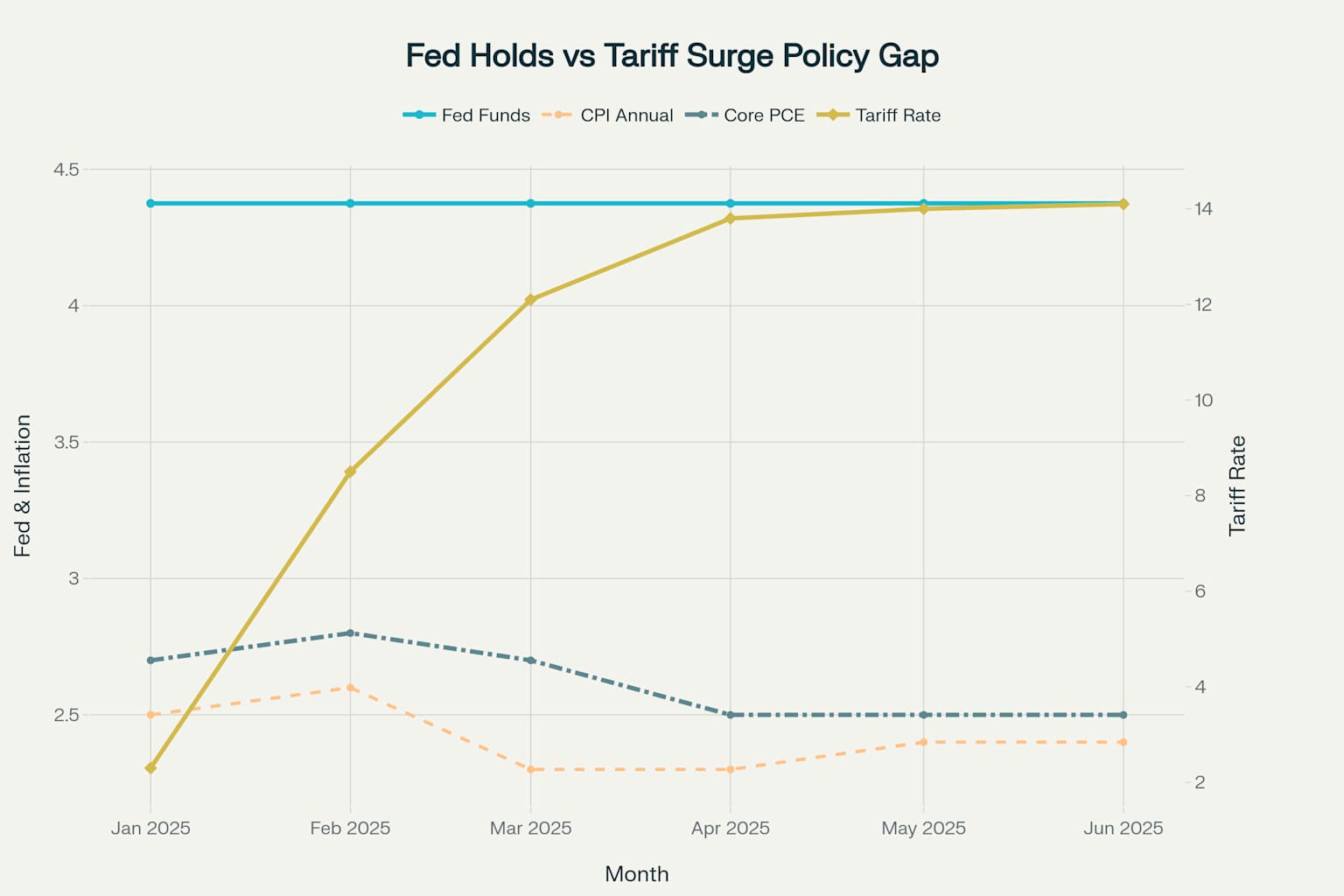

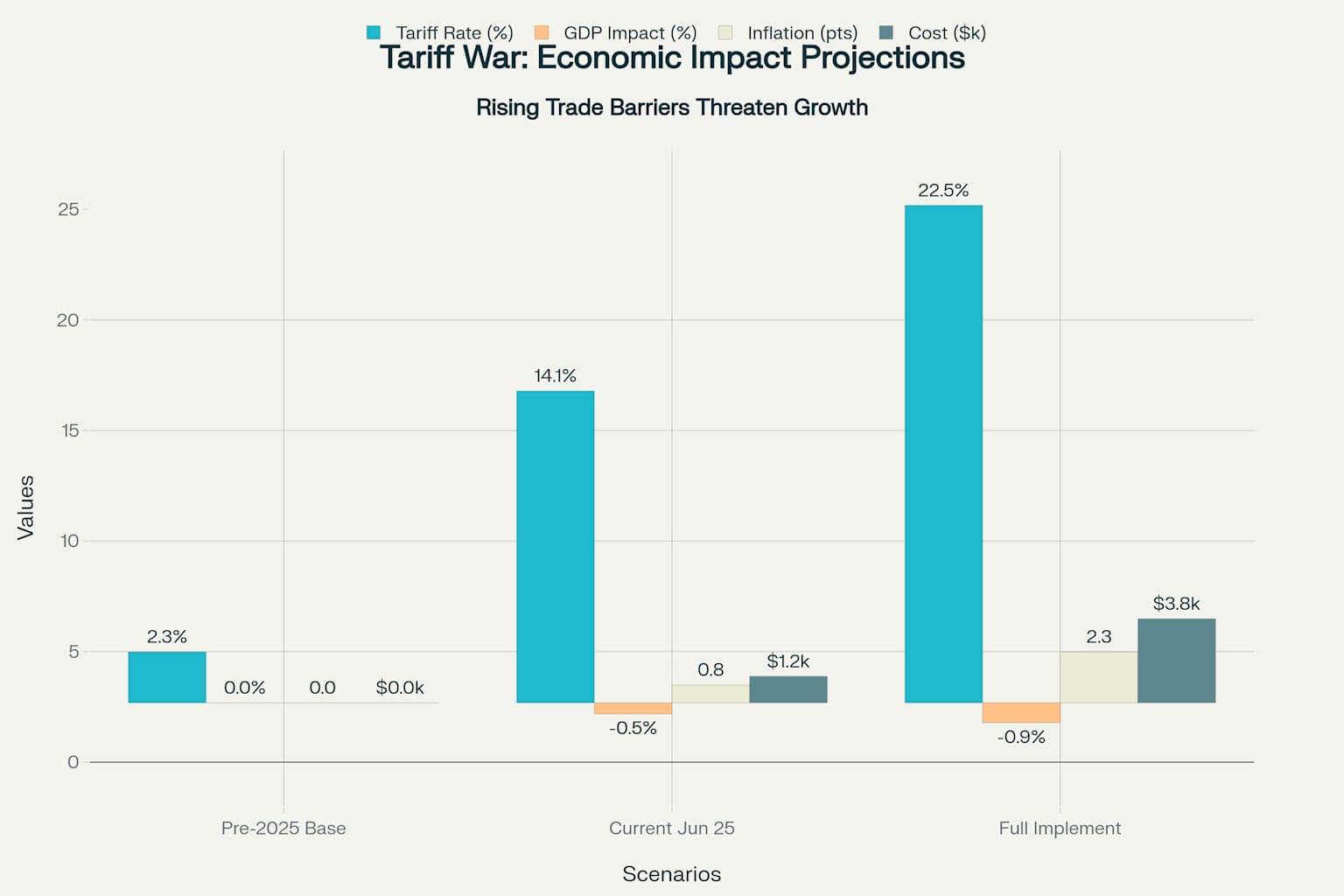

The quantitative evidence of this policy contradiction is overwhelming and alarming. The Federal Reserve has maintained its federal funds rate in the 4.25%-4.50% range since December 2024, even as average effective tariff rates have surged from a baseline of 2.3% to 14.1% by June 2025 – a staggering 514% increase that represents the highest tariff levels since 1941. Core inflation measures remain persistently above the Fed’s 2% target, with core CPI at 2.8% and core PCE at 2.5% as of the latest data.

The magnitude of economic disruption is already evident in corporate earnings reports across multiple sectors. Best Buy lowered its full-year forecasts citing tariff impacts, while Abercrombie & Fitch projects a $50 million profit hit from current tariff levels. Diageo warned of a $150 million annual profit impact, and Target cut growth projections from positive 1% to negative territory. These are not isolated incidents but systematic evidence of supply-side inflationary pressures building throughout the economy.

Economic modeling from leading institutions confirms the mounting risks. Current tariffs alone will raise the price level by 2.3% in the short run, equivalent to $3,800 in annual consumer losses per household if fully implemented. Forecasts show PCE inflation climbing to 2.7%, up 0.2 percentage points from tariff effects alone. If European Union tariffs are added to current measures, the average effective tariff rate could reach 17%.

Historical Precedents Expose the Fed’s Dangerous Path

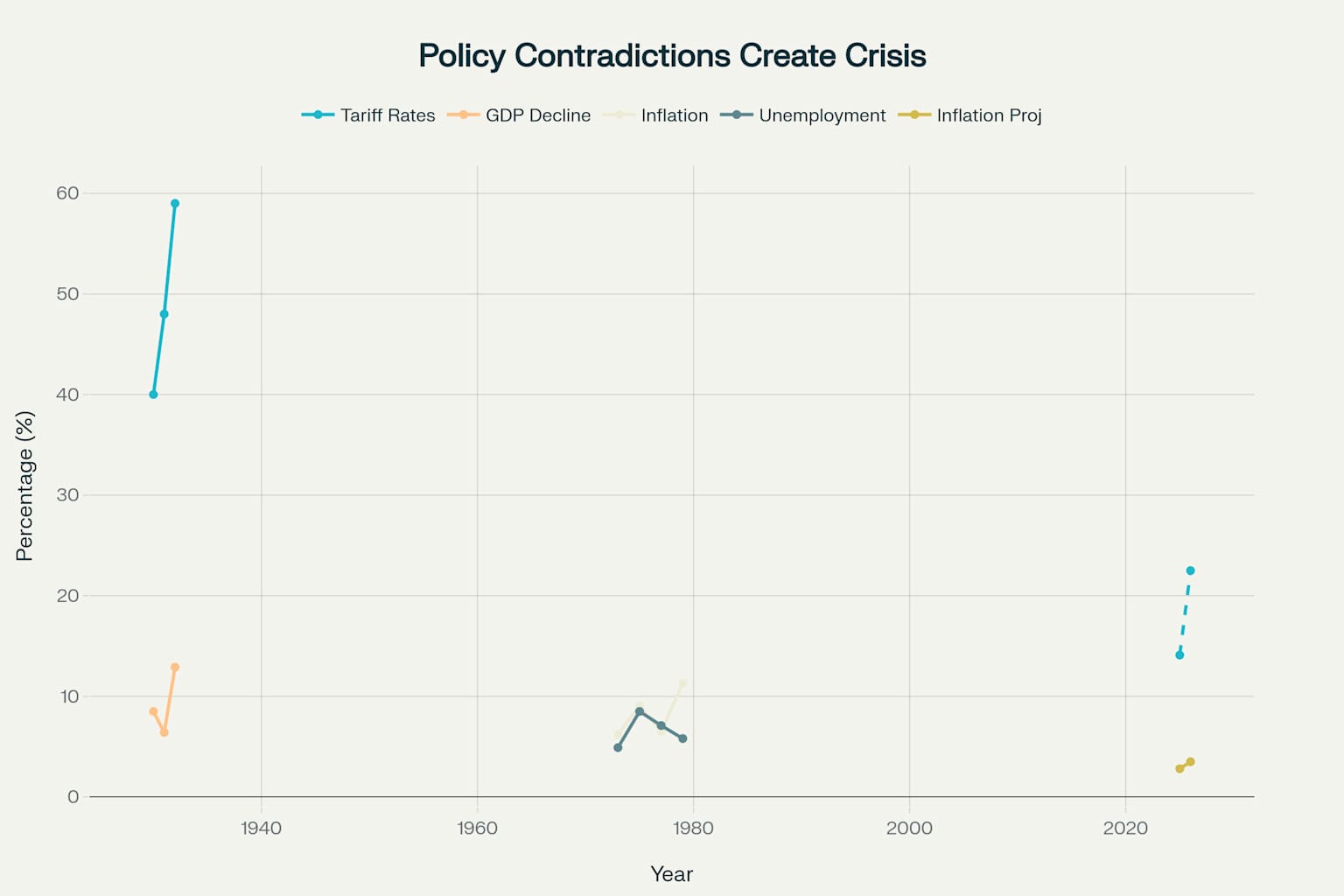

History provides a stark warning about the consequences of policy contradictions during periods of trade disruption. The Smoot-Hawley Tariff Act of 1930 offers the most direct parallel to current conditions. Despite a petition from over 1,000 economists urging President Hoover to veto the legislation, tariff rates rose from 40% to 59% while the economy collapsed. Global trade contracted by two-thirds between 1929 and 1933, and the United States sank deeper into the Great Depression as other nations retaliated with their own protective measures.

The 1970s stagflation period demonstrates what happens when central banks accommodate supply shocks rather than maintain price stability. The Federal Reserve under Arthur Burns attempted to stimulate growth while oil crises drove up input costs, resulting in inflation rates ranging from 6.2% to 11.3% and unemployment reaching 8.5% by 1975. The Fed’s loss of credibility during this period took over a decade to restore and required the painful Volcker shock treatment of the early 1980s.

The current situation bears ominous similarities to both historical episodes. Like the 1930s, we face escalating trade wars with uncertain endpoints and mounting corporate uncertainty about future policy direction. Like the 1970s, the Fed is contemplating monetary accommodation in the face of supply-side inflation pressures. The Federal Reserve’s own Beige Book reported that uncertainty around trade policy became pervasive in April, with mentions of uncertainty spiking to 89 times compared to just 13 times in April 2024.

The Mechanics of Policy Failure

The fundamental problem lies in the timing and transmission mechanisms of tariff-driven inflation versus monetary policy effects. Research shows that tariffs typically impact consumer prices with a two-to-three-month lag. This means the full inflationary effects of tariffs implemented in early 2025 are only beginning to manifest in consumer price indices. Meanwhile, rate cuts would take six to twelve months to meaningfully impact economic activity, creating a dangerous temporal mismatch.

New Keynesian models of optimal monetary policy responses to tariff shocks consistently demonstrate that expansionary policy in response to trade disruptions amplifies rather than mitigates inflationary pressures. The optimal monetary response to tariffs is actually contractionary, not expansionary, as central banks must offset the direct inflationary impact to maintain price stability. The Fed’s current contemplation of rate cuts represents a textbook example of policy error according to established macroeconomic theory.

The empirical evidence from corporate behavior confirms these theoretical predictions. Companies are not just raising prices but actively postponing investments due to policy uncertainty. Military equipment manufacturers have delayed expansion plans, while general manufacturing sectors have put investments on hold pending clarity on future trade policy. This investment decline will reduce productivity growth and further embed inflationary pressures into the economic structure.

Addressing and Refuting the Counterarguments

Proponents of rate cuts argue that tariffs represent a one-time price level increase rather than ongoing inflation, suggesting monetary accommodation is appropriate to offset recessionary effects. This view, expressed by some Fed officials, fundamentally misunderstands the dynamic nature of trade wars and inflation expectations.

The “one-time price increase” argument fails on multiple empirical grounds. First, current tariffs are not static but escalating, with additional measures threatened against European Union imports that could push effective rates to 17% or higher. Second, the tariff structure itself creates ongoing adjustment costs as supply chains reorganize and companies substitute between domestic and foreign inputs. Third, and most critically, business surveys show companies planning additional price increases throughout 2025 as they absorb the full impact of trade policy changes.

The inflation expectations channel represents perhaps the greatest risk. Five-year breakeven inflation expectations have remained elevated around 2.33%, above historical norms, suggesting markets are pricing in persistent price pressures. Rate cuts in this environment would signal that the Fed prioritizes short-term growth over price stability, potentially triggering a de-anchoring of inflation expectations similar to the 1970s experience.

Financial market volatility provides additional evidence against the accommodation argument. The VIX spiked following April tariff announcements, and a 20% effective tariff increase could reduce GDP growth by 2-2.5 percentage points while triggering a shallow recession. In this context, rate cuts would likely prove ineffective at stimulating demand while amplifying inflation risks – the worst of both worlds for monetary policy.

The Stagflationary Trap Ahead

The Federal Reserve now faces the prospect of entering a stagflationary trap of its own making. Economic forecasts project US GDP growth slowing to just 1.7% in 2025, down from 2.8% in 2024, while inflation pressures mount. The European Central Bank has noted that disconnects between financial market volatility and economic policy uncertainty become more pronounced when policy contradictions emerge.

The transmission mechanisms that made monetary policy effective during previous cycles have been fundamentally altered by the tariff regime. Traditional interest rate channels work by affecting borrowing costs and investment decisions, but current corporate behavior shows businesses prioritizing tariff-related cost management over expansion decisions. Rate cuts cannot offset supply-side cost increases and may actually worsen resource allocation by encouraging malinvestment in import-competing sectors.

International spillover effects compound these domestic risks. Trading partners have already begun retaliatory measures, and further US monetary accommodation could trigger currency wars that amplify trade tensions. The European Central Bank has explicitly warned about financial market volatility stemming from US policy uncertainty. Rate cuts would likely weaken the dollar, making imports more expensive and further embedding inflationary pressures into the US economy.

The Path Forward: Policy Coherence Over Political Expedience

The Federal Reserve must abandon its rate cut considerations and maintain current policy rates until tariff-driven inflation pressures subside. Chairman Powell’s own admission that Fed projections are for inflation to move up because of tariffs should preclude any monetary accommodation until these effects are fully absorbed. The central bank’s dual mandate requires prioritizing price stability when supply-side shocks threaten to de-anchor inflation expectations.

Alternative policy frameworks, such as nominal GDP targeting, offer superior approaches to navigating the current environment. Under NGDP targeting, the Fed would focus on total spending growth rather than attempting to fine-tune inflation and employment separately. This approach would automatically accommodate one-time price level increases from tariffs while preventing the policy contradictions that have characterized recent Fed communications.

The institutional credibility of the Federal Reserve itself is at stake. Political pressure from the White House for rate cuts, combined with dovish signals from some Fed officials, threatens the independence that is crucial for effective monetary policy. Historical analysis shows that central bank independence is essential for maintaining low inflation expectations and economic stability.

Conclusion: A Reckoning with Reality

The Federal Reserve’s consideration of rate cuts amid escalating tariff wars represents a fundamental misunderstanding of both economic theory and historical experience. The central bank appears poised to repeat the policy errors of the 1970s by accommodating supply-side inflation pressures rather than maintaining price stability. The quantitative evidence is unambiguous: current tariffs are already imposing significant economic costs, and further monetary accommodation will either prove ineffective against these headwinds or fuel an inflationary spiral that damages long-term economic growth.

Chairman Powell’s testimony this week exposed the intellectual bankruptcy of current Fed thinking. Acknowledging that tariffs will drive inflation while simultaneously considering rate cuts reveals a central bank that has lost its policy compass. The Federal Reserve must choose between political expedience and economic reality – it cannot have both without devastating consequences for American prosperity.

The stakes could not be higher. As former St. Louis Fed President James Bullard warned, the current trajectory dramatically raised the risk of outcomes similar to the Great Depression. The Federal Reserve has the tools and institutional authority to prevent this outcome, but only if it abandons its dangerous rate cut gamble and returns to the fundamental principle that price stability must come first. History will judge harshly a central bank that chose political accommodation over economic responsibility at this critical juncture.

Editor’s Note: This is an opinion column and represents the views of the author. It does not necessarily reflect the views of this publication.