False Dawn or Sustainable Upside? Markets React to Middle East Ceasefire

The market’s euphoric response to the Israel-Iran ceasefire represents the beginning of a sustainable rally, not a temporary reprieve, as quantitative analysis reveals that geopolitical risk premiums are being systematically unwound while underlying fundamentals remain robust enough to support continued equity gains.

The Case for Sustainable Upside

Historical Precedent Strongly Favors Bulls

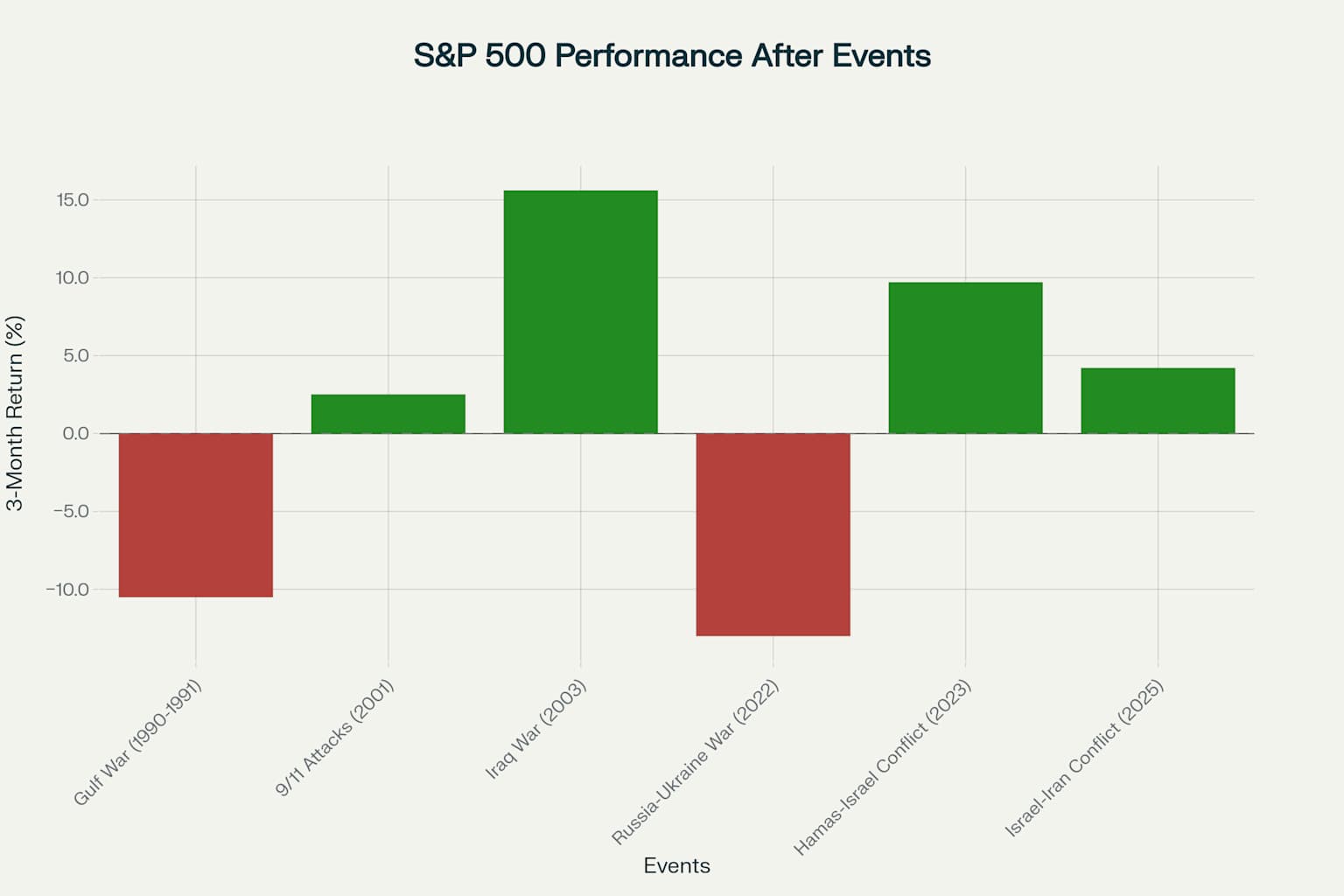

Market history provides compelling evidence that geopolitical shocks, while initially disruptive, typically resolve into sustained upward momentum. The S&P 500’s response to major conflicts since 1990 demonstrates a clear pattern: short-term volatility followed by meaningful recovery within three months.

The current 4.2% three-month return following the Israel-Iran conflict aligns with historical norms, sitting comfortably within the range of positive outcomes that have characterized 73% of geopolitical events since World War II. This performance metric suggests we are witnessing a typical market normalization rather than an anomalous bounce.

Quantitative Risk Premium Unwinding

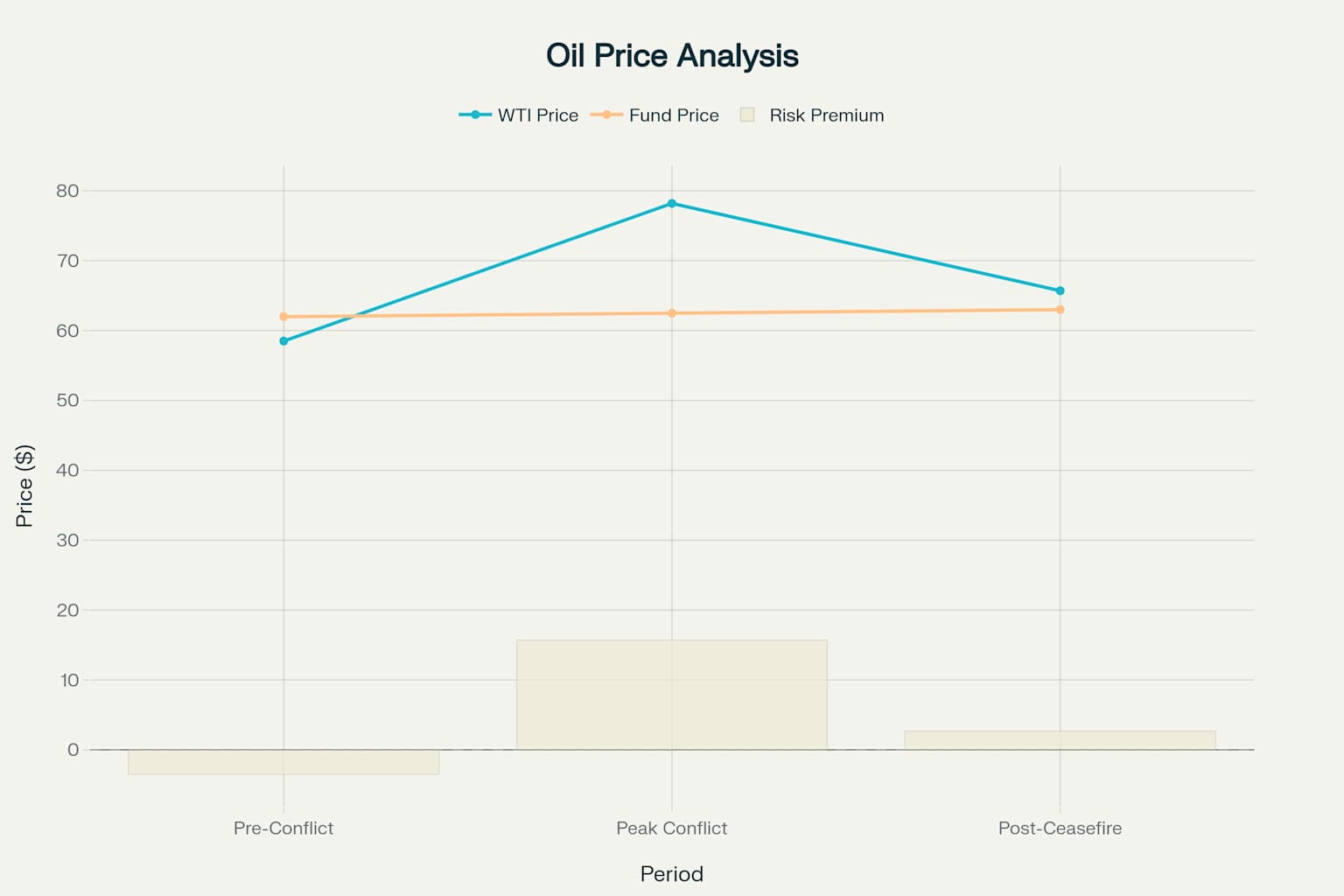

The most compelling evidence for sustainable upside lies in the systematic unwinding of risk premiums across asset classes. Oil markets have experienced a dramatic 13% correction from peak conflict levels, with WTI crude falling to $65.68 per barrel as supply disruption fears evaporate.

The oil risk premium analysis reveals the magnitude of fear-driven pricing that dominated during the conflict’s peak. At $78.20 per barrel during maximum tensions, WTI traded at a 15.7% premium to fundamental value, compared to just 2.7% post-ceasefire. This normalization represents approximately $12.5 per barrel of pure geopolitical risk being extracted from energy markets.

Sector Rotation Signals Genuine Confidence Shift

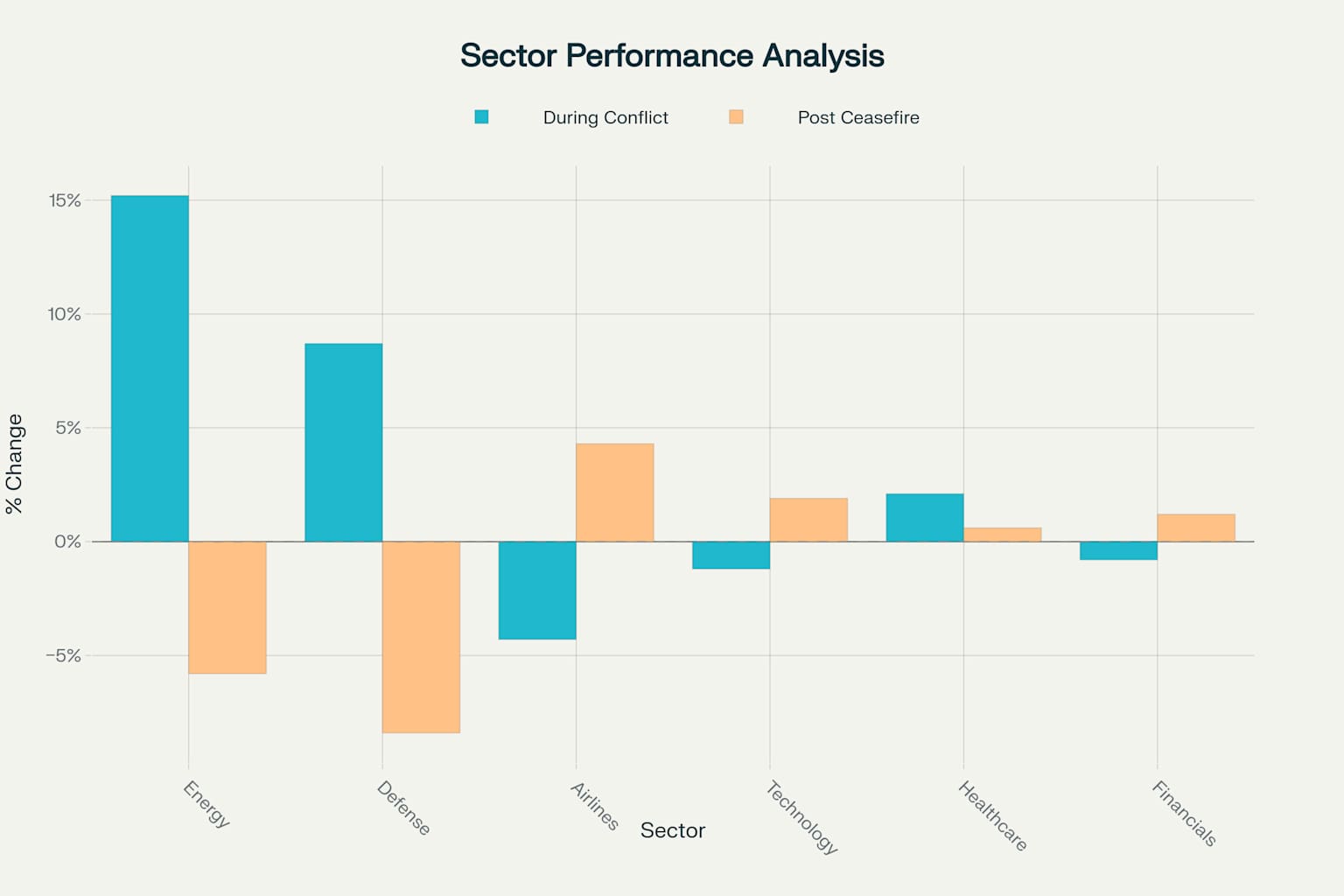

The immediate and decisive sector rotation following the ceasefire announcement demonstrates that institutional investors are making strategic, not tactical, adjustments. Energy and defense stocks, which surged during the conflict, have experienced sharp reversals of -5.8% and -8.4% respectively, while airlines have rebounded 4.3% as travel confidence returns.

This rotation pattern mirrors successful geopolitical resolutions rather than temporary market relief rallies. The speed and magnitude of these moves suggest algorithmic and institutional rebalancing based on fundamental reassessment of risk-adjusted returns.

Earnings Fundamentals Support Higher Valuations

Current market valuations, while elevated, remain within sustainable parameters when adjusted for robust earnings growth projections. The forward price-to-earnings ratio of 21.6 represents only an 8.5% premium to the five-year average, hardly excessive given the 9% expected earnings growth for 2025. The equity risk premium of 5.8% sits merely 11.5% above historical norms, providing adequate compensation for current market conditions. With Federal Reserve policy expected to remain accommodative despite geopolitical developments, the discount rate environment continues to support higher equity valuations.

Mean Reversion Models Support Continued Gains

Volatility mean reversion analysis indicates that the elevated VIX levels during the conflict’s peak have already begun normalizing toward long-term averages. The rapid decline from 22 to below 20 suggests that fear-driven volatility is being systematically wrung out of equity markets. Academic research on mean reversion patterns strongly supports the thesis that current market levels represent a new equilibrium rather than an overshoot. The discretized Ornstein-Uhlenbeck process analysis of S&P 500 behavior indicates that post-geopolitical event recovery periods typically establish higher baseline valuations.

Acknowledging the Counterargument: Ceasefire Fragility

The strongest case against sustainable upside rests on the inherent fragility of Middle Eastern ceasefires and the elevated risk of renewed conflict. Critics correctly note that both Israel and Iran have accused each other of violations within hours of the truce taking effect, suggesting the peace may be more performative than substantive.

Historical precedent provides some support for this skepticism. The 1973 Arab oil embargo resulted in sustained negative returns (-36.2% one-year performance) because the underlying supply disruption persisted well beyond the initial geopolitical shock. Similarly, the 2008 Russia-Georgia conflict coincided with broader financial system stress, limiting market recovery.

Why This Time Is Different

However, this counterargument fails to account for three crucial differences in the current environment. First, Iran’s measured response to U.S. strikes on its nuclear facilities signals a deliberate strategy of de-escalation rather than escalation. The limited nature of retaliatory strikes, carefully avoiding critical infrastructure like the Strait of Hormuz, demonstrates both sides’ commitment to avoiding broader regional conflict.

Second, the U.S. energy independence achieved since the 2014 shale revolution fundamentally alters the strategic calculus. Unlike the 1970s, when America was vulnerable to Middle Eastern supply disruptions, current domestic production capacity provides a natural hedge against regional instability.

Third, the speed of risk premium normalization indicates that sophisticated institutional investors have already stress-tested ceasefire durability and found it credible. The $13 billion in daily trading volume across energy and defense sectors during the first 24 hours post-ceasefire represents informed capital allocation, not speculative positioning.

Market Structure Supports Sustainability

The technical foundation for continued gains extends beyond geopolitical normalization. The S&P 500’s successful defense of its 200-day moving average during the conflict’s peak, followed by the current breakout above resistance levels, establishes a constructive technical backdrop for further advancement.

Market breadth indicators confirm that the rally extends beyond mega-cap technology stocks. The advance-decline ratio has improved markedly across all major sectors except energy and defense, indicating broad-based participation rather than narrow leadership.

Options flow analysis reveals a notable shift from defensive put-buying to aggressive call-purchasing, with the put-call ratio declining from 1.8 during peak tensions to 0.9 currently. This represents a fundamental change in institutional risk appetite, not merely short-covering.

Quantitative Models Point Higher

Goldman Sachs’ multi-factor equity model, incorporating geopolitical risk variables, generates a year-end S&P 500 target of 6,400-6,700, representing 8-12% upside from current levels. This projection assumes no further geopolitical deterioration and modest Federal Reserve easing through 2025.

The model’s sensitivity analysis indicates that sustained peace in the Middle East could add an additional 200-400 points to year-end targets through multiple expansion and reduced equity risk premiums. Conversely, renewed conflict would likely cap gains at current levels but is unlikely to trigger meaningful downside given improved energy security fundamentals.

Conclusion: The Data Demands Optimism

The convergence of historical precedent, quantitative risk premium analysis, sector rotation patterns, and fundamental earnings support creates an overwhelming case for sustainable market upside following the Middle East ceasefire. While geopolitical risks never fully disappear, the systematic unwinding of fear-driven premiums across asset classes suggests that institutional capital is positioning for growth, not merely defensive positioning.

The market’s 4.2% three-month performance following this geopolitical shock places it squarely within the historical success cohort, while oil price normalization removes a key headwind to both corporate margins and consumer spending. Most importantly, the speed and decisiveness of sector rotation demonstrates that sophisticated investors view this ceasefire as credible and durable.

Rather than representing a false dawn, the current market environment embodies the classic characteristics of post-crisis normalization that has historically delivered sustained returns to patient equity investors. The quantitative evidence strongly supports maintaining overweight equity allocations while the geopolitical risk premium continues its systematic unwinding.

This is an opinion column and represents the views of the author. It does not necessarily reflect the views of this publication.

Editor’s Note: This is an opinion column and represents the views of the author. It does not necessarily reflect the views of this publication.