Fed Holds Off Rate Cuts as Tariff Fallout Looms

The Federal Reserve’s decision to maintain interest rates at their current levels represents a calculated response to an unprecedented economic landscape. As the central bank navigates the intersection of persistent inflationary pressures, expansive trade policies, and mounting fiscal deficits, policymakers face a complex balancing act that defies conventional monetary policy frameworks. The Federal Open Market Committee’s unanimous decision to hold the federal funds rate steady at 4.25-4.50% for the fourth consecutive meeting signals a marked departure from historical patterns of monetary accommodation during periods of economic uncertainty.

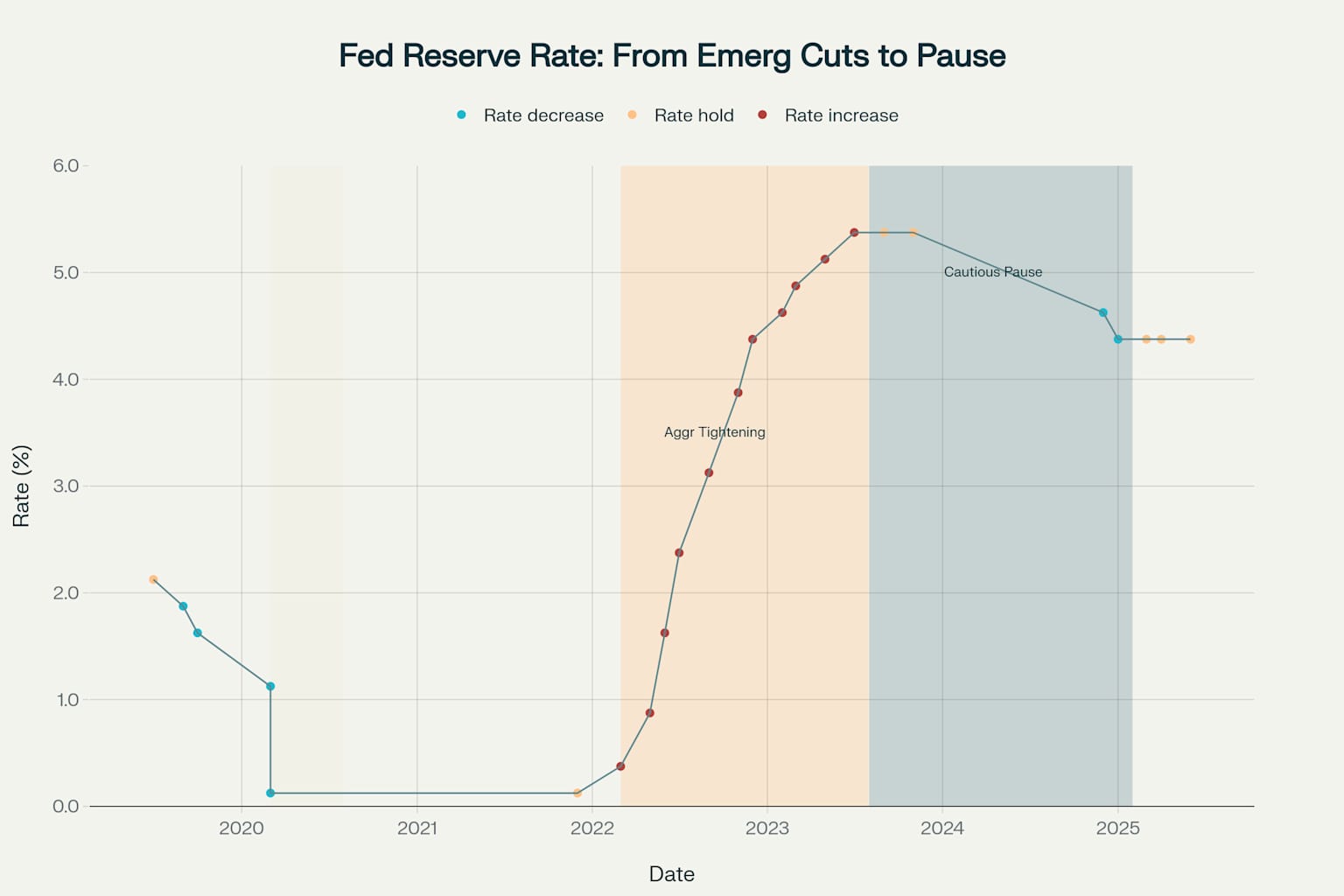

Federal Reserve interest rate trajectory showing the shift from emergency pandemic cuts to aggressive tightening, followed by the current cautious pause amid economic uncertainty

The Tariff Challenge: Inflationary Pressures Mount

The Trump administration’s comprehensive tariff strategy has introduced significant complexity into the Federal Reserve’s decision-making calculus. The implementation of a 10% tariff on all imports, combined with elevated rates of 30% on Chinese goods, represents the largest trade policy intervention since the 1930s. These measures are projected to generate $156.4 billion in federal tax revenues during 2025, equivalent to 0.51% of GDP, making them the largest tax increase since 1993.

Analysis of tariff impacts showing the relationship between trade volumes and estimated price effects across different regions and countries

The inflationary impact of these tariffs extends beyond simple pass-through effects. Economic analysis indicates that tariffs create sustained inflationary pressures through multiple channels, including profit-led price increases, wage inflation, reduced market competition, and supply chain disruptions. The Penn Wharton Budget Model projects that comprehensive tariff implementation will reduce long-term GDP by approximately 6% and wages by 5%, while creating lifetime losses of $22,000 for middle-income households.

Current data demonstrates that tariff effects are already materializing in consumer prices. Retailers including Walmart have confirmed price increases due to tariff implementation, with some Chinese imports experiencing price jumps exceeding 100%. The Federal Reserve’s preferred inflation measure, core Personal Consumption Expenditures (PCE), reached 2.5% in April 2025, well above the central bank’s 2% target.

Economic Projections: A Stagflationary Scenario Emerges

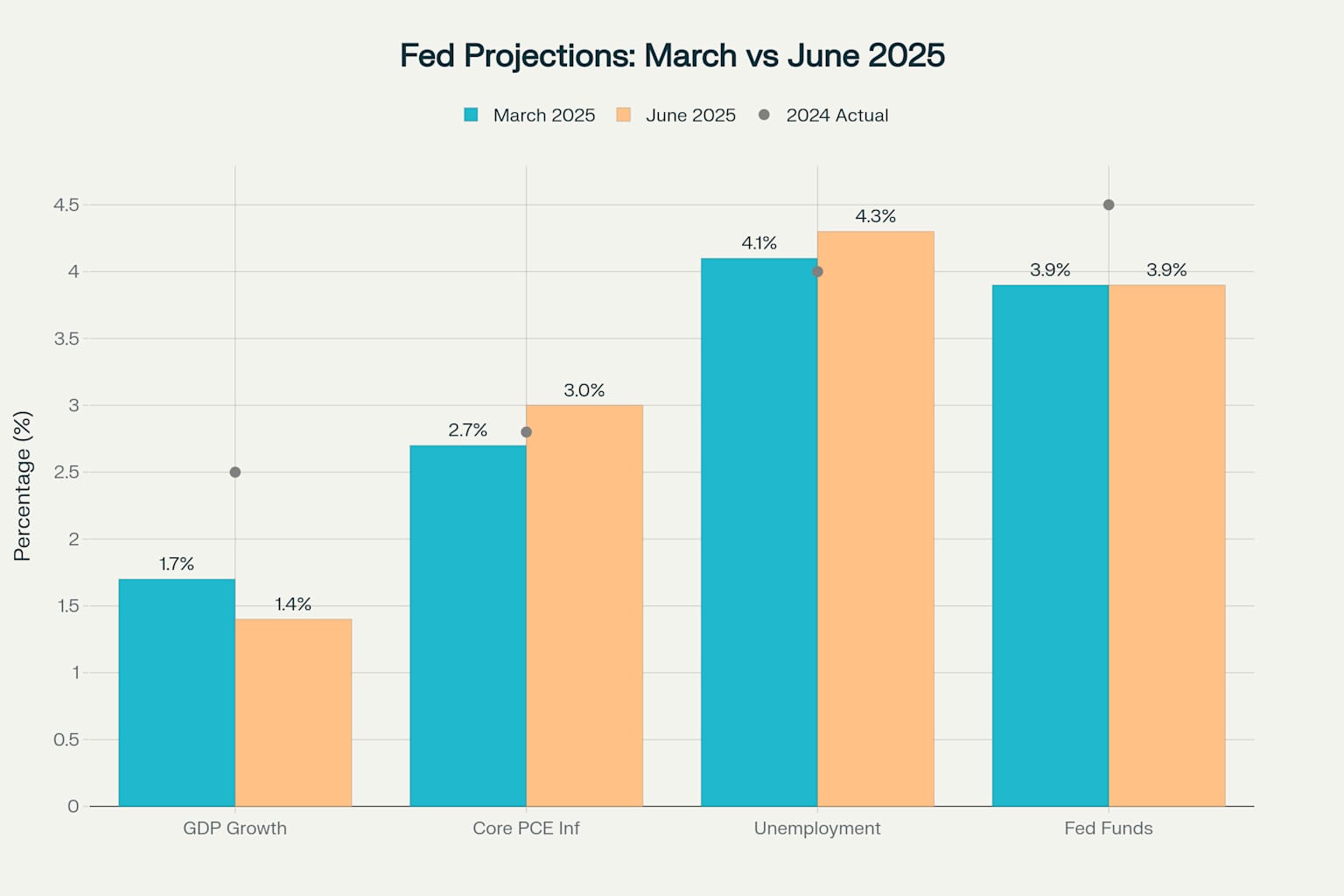

The Federal Reserve’s latest economic projections reveal a marked deterioration in the growth-inflation trade-off. Between March and June 2025, Fed officials revised their GDP growth forecast downward from 1.7% to 1.4%, while simultaneously increasing their inflation projection from 2.7% to 3.0%. This combination of slower growth and higher inflation represents classic stagflationary conditions that present no clear policy response.

Federal Reserve economic projections showing downward revisions to growth and upward revisions to inflation between March and June 2025

The unemployment rate projection has also increased from 4.1% to 4.3%, suggesting that labor market conditions will soften even as inflationary pressures persist. These revisions reflect the Federal Reserve’s assessment that tariff policies will weigh on economic activity while simultaneously elevating price levels. Fed Chair Jerome Powell emphasized that policy changes remain evolving, with consequences depending heavily on final tariff levels and implementation details.

Global economic organizations have corroborated these concerns. The International Labour Organization revised global GDP growth downward from 3.2% to 2.8% for 2025, citing persistent geopolitical tensions, trade disruptions, and heightened uncertainty. Approximately 84 million workers across 71 countries face elevated disruption risks due to higher tariffs and trade uncertainty affecting US consumer demand.

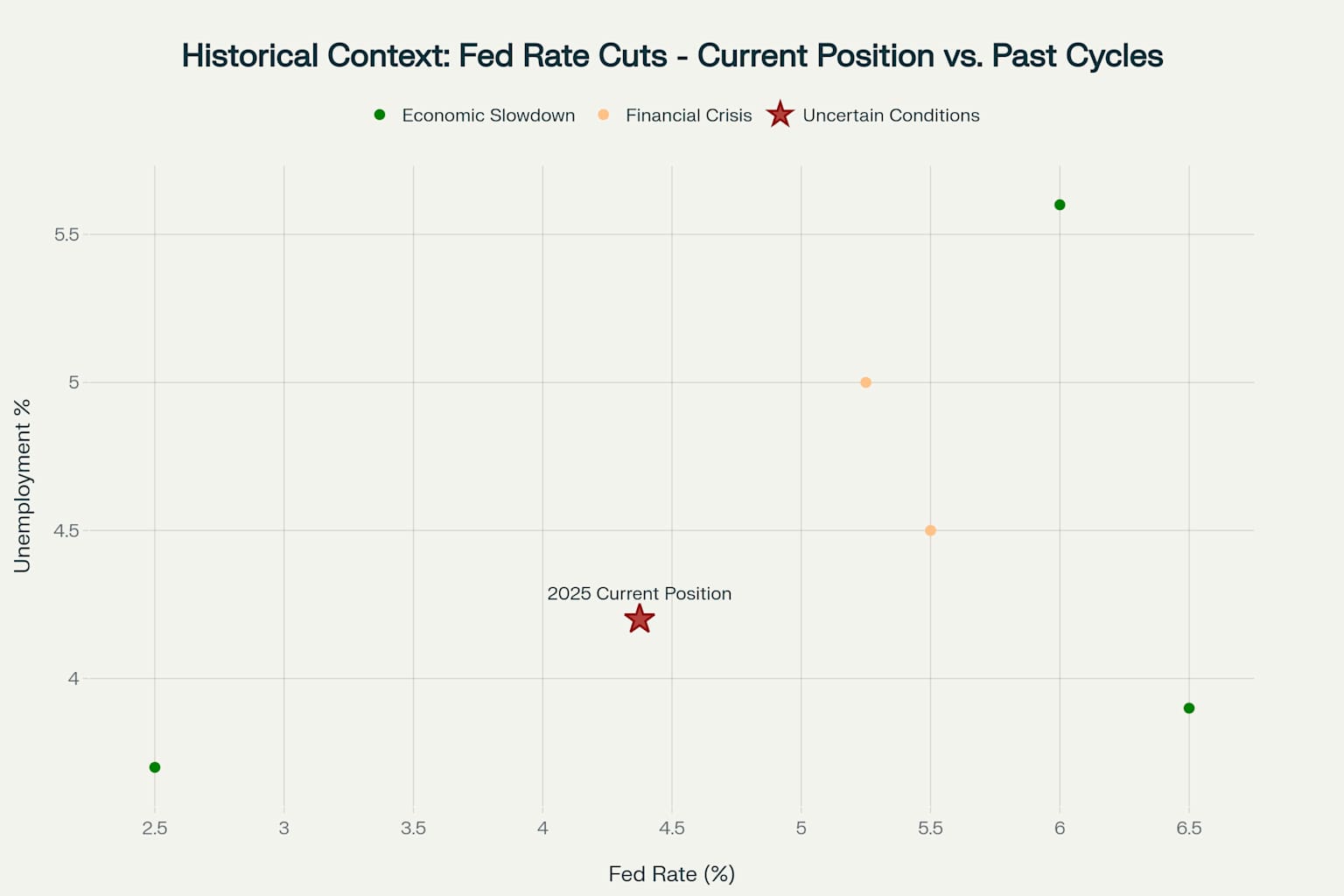

Historical Context: An Unprecedented Policy Position

The current monetary policy stance represents a historical anomaly when compared to previous Federal Reserve rate-cutting cycles. Analysis of cutting cycles since 1994 reveals that 92% of rate cuts occurred from higher initial levels than the current 4.375% midpoint. Nearly 99% of historical cuts took place when unemployment exceeded current levels, and 65% occurred during periods of higher inflation.

Historical comparison of Federal Reserve rate cutting cycles showing how the current position differs from past patterns

The Federal Reserve has implemented 140 rate cuts since 1960, averaging 23 cuts per decade. However, no rate cuts occurred during the 2010s decade due to the extended zero-interest-rate policy following the 2008 financial crisis. The current situation presents unique challenges: rates remain elevated compared to post-crisis norms, yet economic conditions do not clearly warrant aggressive accommodation.

Previous cutting cycles typically responded to clear catalysts: economic recessions, financial crises, or pronounced economic slowdowns. The 2025 environment features persistent inflation above target, moderate unemployment, and trade-policy-induced uncertainty that creates ambiguous signals for monetary policy direction.

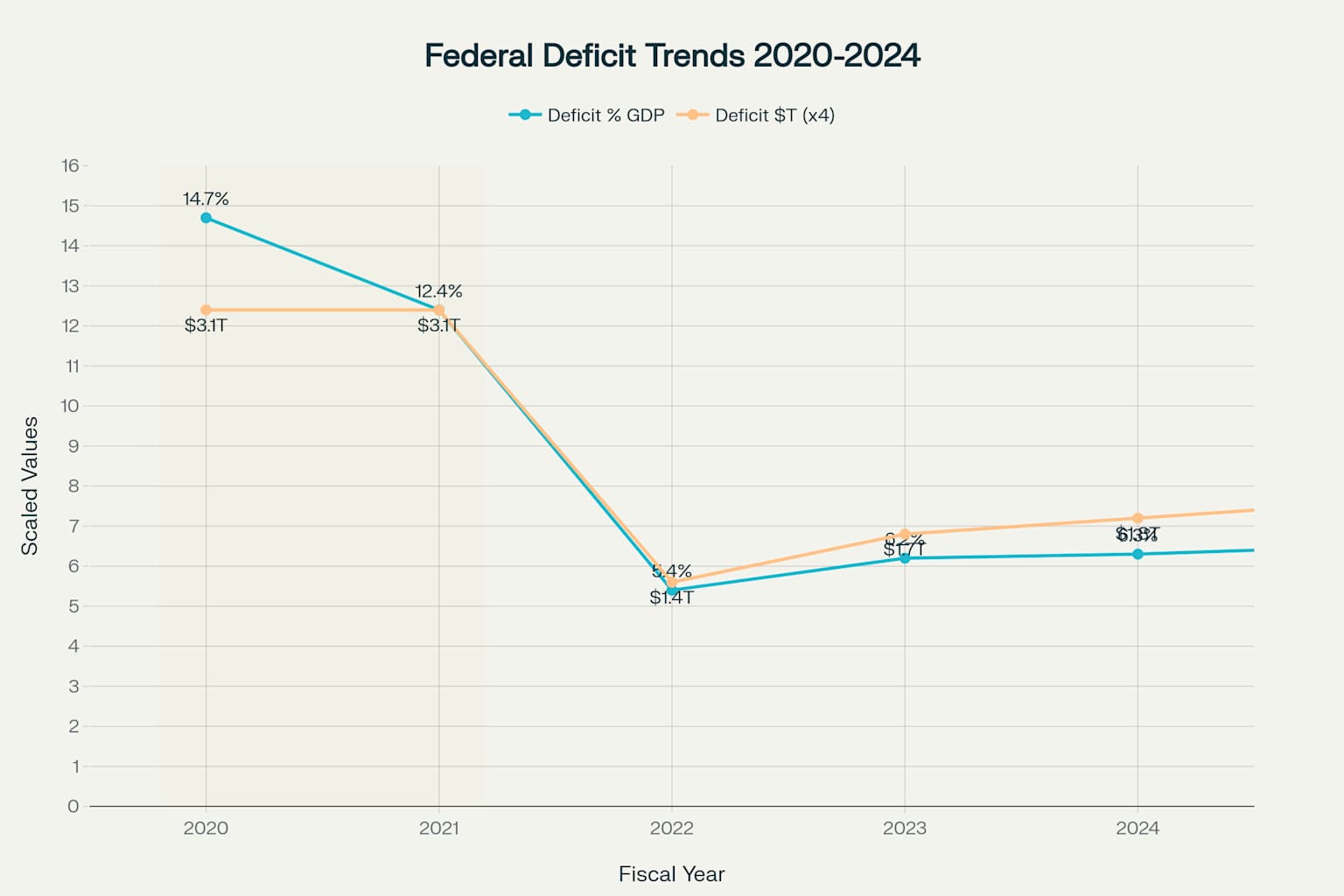

Fiscal Pressures: Deficits Persist Despite Recovery

The federal government’s fiscal position adds another layer of complexity to Federal Reserve decision-making. Despite economic recovery from pandemic lows, the federal deficit remains elevated at $1.9 trillion for fiscal year 2025, representing 6.5% of GDP. This deficit level significantly exceeds historical norms for periods of full employment and peacetime conditions.

Federal deficit trends from 2020-2025 showing persistent fiscal pressures with deficit remaining at 6.5% of GDP despite economic recovery

The 12-month rolling deficit reached $2.0 trillion as of April 2025, representing 6.9% of GDP compared to 5.8% in the previous year. Revenue collections have increased due to tariff receipts, with customs duties rising by $17 billion in April 2025 compared to the previous year. However, these gains are offset by continued spending growth and interest payments on accumulated debt.

Congressional Budget Office projections indicate that without policy changes, the debt-to-GDP ratio will grow from 100% in 2024 to 190% by 2050. This trajectory suggests that fiscal policy will provide limited support for economic stabilization, placing greater responsibility on monetary policy for macroeconomic management.

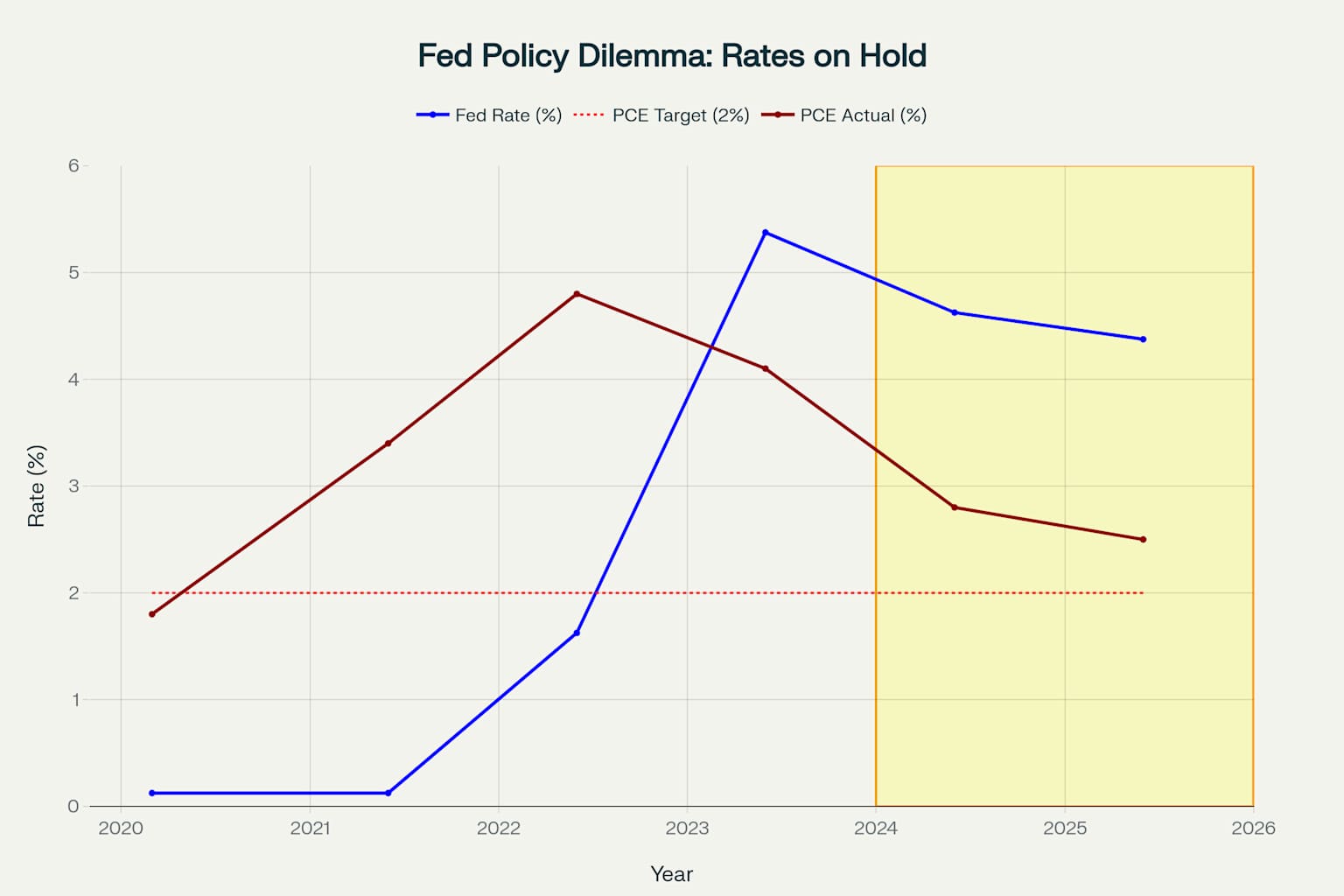

The Independence Factor: Political Pressure and Policy Credibility

Federal Reserve independence faces renewed testing as political pressure for rate cuts intensifies. President Trump has repeatedly criticized Fed Chair Powell, demanding immediate rate reductions and expressing frustration with the central bank’s cautious approach. Recent social media posts have called for Congressional action against what the President termed a “very dumb, hardheaded person.”

Federal Reserve policy dilemma showing rates held steady despite economic uncertainty and inflation above target

Research demonstrates that central bank independence yields significant long-term benefits for inflation control. Empirical analysis shows that improvements in central bank independence create lasting effects, with greater impact on inflation in the long run compared to short-term adjustments. Central bank independence also reduces inflation persistence, enhancing monetary policy effectiveness.

The Federal Reserve’s commitment to data-dependent decision-making reflects this independence principle. Powell emphasized that policymakers remain “well positioned to wait for additional information about the probable direction of the economy before contemplating any modifications to our policy approach.”

Market Expectations and Forward Guidance

Financial markets currently anticipate limited Federal Reserve accommodation, with the central bank’s dot plot indicating two quarter-point cuts by year-end 2025. However, seven of nineteen FOMC members now project no rate cuts for 2025, compared to four in March. This increasing hawkishness among committee members reflects growing uncertainty about the inflation outlook.

The Federal Reserve faces a communication challenge in managing market expectations while maintaining policy flexibility. Forward guidance becomes complicated when economic conditions feature multiple competing pressures that create ambiguous signals for policy direction. The central bank’s emphasis on patience and data-dependence represents an attempt to preserve options while economic clarity emerges.

Quantitative Analysis: Models Under Stress

Traditional monetary policy models struggle to provide clear guidance in the current environment. The standard Taylor Rule framework, which relates interest rates to inflation gaps and output gaps, generates conflicting signals when inflation exceeds target while growth slows simultaneously. New Keynesian models that incorporate heterogeneous agents (HANK models) provide additional insights into distributional effects but do not resolve the fundamental policy trade-offs.

The Federal Reserve’s own modeling approaches acknowledge significant uncertainty. The central bank’s statement noted that “uncertainty about the economic outlook has diminished but remains elevated,” reflecting the challenges of forecasting in an environment shaped by evolving trade policies and their complex economic interactions.

Economic research on tariff effects indicates that many traditional trade and macroeconomic models fail to capture the full harm caused by large-scale tariff implementation. The reduction in economic openness, including international capital flows, creates effects that extend beyond simple price adjustments and require more sophisticated analytical frameworks.

Conclusion: Navigating Uncharted Territory

The Federal Reserve’s cautious approach to rate cuts reflects the extraordinary complexity of current economic conditions. The combination of trade-policy-induced inflationary pressures, persistent fiscal deficits, and uncertain growth prospects creates a policy environment without clear historical precedent. The central bank’s decision to maintain rates steady represents a prudent response to multiple competing risks rather than a single dominant economic concern.

The stagflationary scenario emerging from Fed projections suggests that traditional monetary policy tools may prove insufficient for addressing simultaneous growth and inflation challenges. The persistence of elevated deficits further constrains policy options by limiting fiscal support for economic stabilization. These conditions require careful navigation that prioritizes long-term credibility over short-term accommodation.

The Federal Reserve’s emphasis on data-dependence and patience reflects recognition that premature policy adjustments could exacerbate existing imbalances. As tariff effects continue to unfold and fiscal pressures persist, the central bank’s measured approach provides time for economic relationships to clarify before committing to a particular policy direction. The ultimate success of this strategy will depend on the evolution of trade policies, inflation dynamics, and the broader economic response to these unprecedented policy combinations.